BHP Group Limited (BHP.AX) Hits Record Highs Amid Strategic Copper Pivot

BHP Group Limited (BHP.AX) reached a significant milestone on 11 May 2026, with its share price ascending to an all-time high of 59.78 AUD. This peak represents a 2.9% single-day increase and follows a sustained period of appreciation driven by record-high copper prices and a successful strategic realignment toward commodities essential for the global energy transition. The company, currently valued at approximately AU$305 billion, has solidified its position as the premier global diversified miner, leveraging its low-cost iron ore operations to fund a massive expansion into copper and potash. This transition is increasingly reflected in the company's earnings profile, where copper has emerged as the primary driver of growth, capitalising on structural deficits in the global market.

Company Overview

BHP Group Limited (BHP.AX) operates as a global leader in the mining and metals sector, maintaining a dominant presence in the seaborne iron ore market while simultaneously holding the title of the world's largest copper producer. The organisation's portfolio is heavily weighted toward high-quality assets in stable jurisdictions, primarily Australia and the Americas. By market capitalisation, BHP Group Limited (BHP.AX) remained the top-ranked mining entity globally in 2025, a position supported by its scale and operational efficiency. The company's core operations are centred on iron ore, copper, and metallurgical coal, though it is currently undergoing a multi-year programme to pivot toward "future-facing" commodities. This involves significant investment in the Jansen potash project and an aggressive expansion of its copper mineral resources to meet the rising demand from electrification, artificial intelligence, and data centre infrastructure.

Financial Metrics

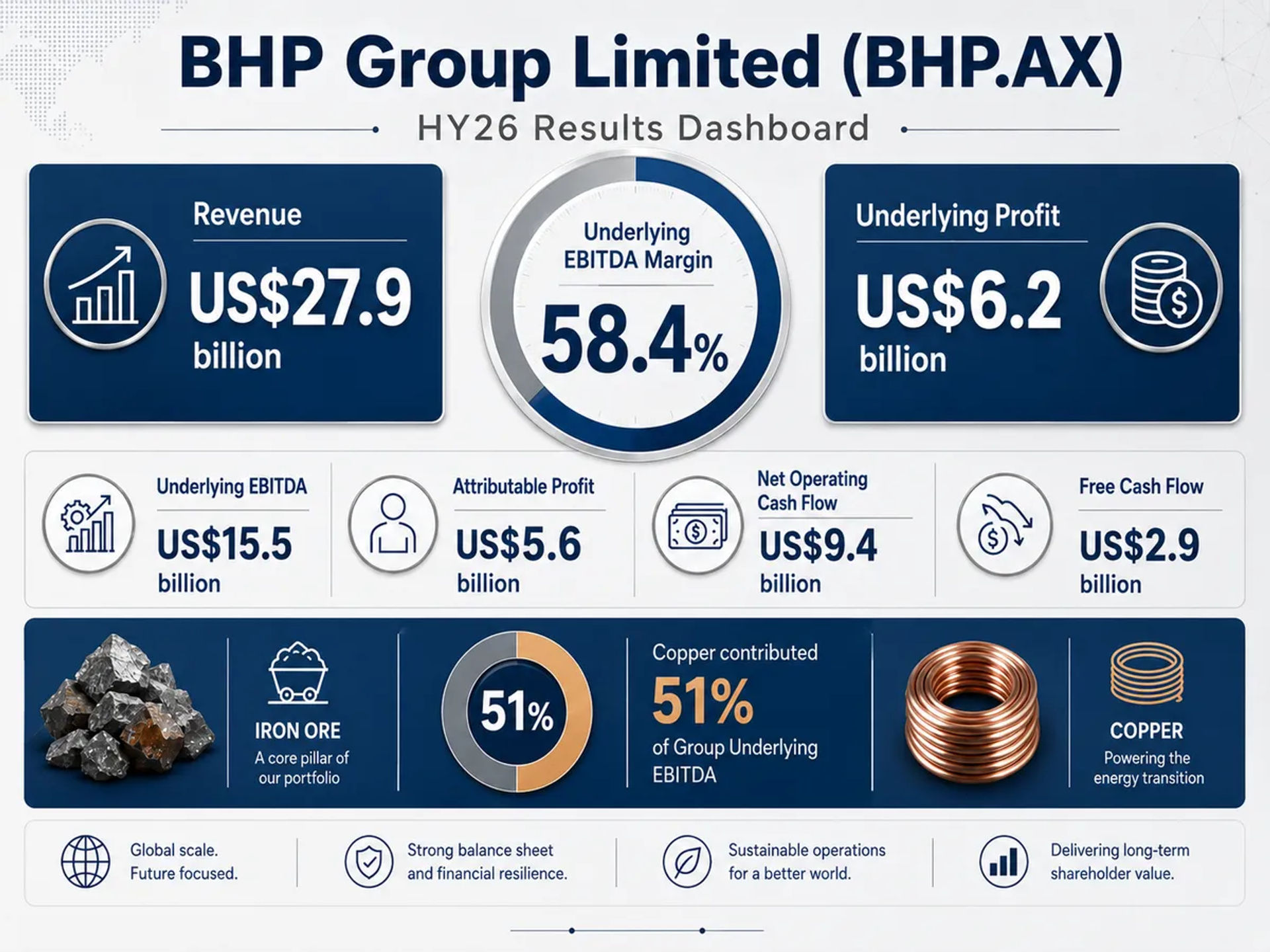

The financial performance for the half-year ended 31 December 2025 (HY26) demonstrates the efficacy of the company's current operational strategy. BHP Group Limited (BHP.AX) reported revenue of US$27.9 billion, marking an 11% increase compared to the prior corresponding period. This top-line growth translated into a substantial 22% rise in underlying attributable profit, which reached US$6.2 billion. A critical highlight of the HY26 results was the contribution of the copper segment, which accounted for 51% of Underlying EBITDA, surpassing iron ore as the primary earnings driver. The company maintained a robust Underlying EBITDA margin of 58.4%, reflecting its status as a low-cost producer even in an environment of fluctuating input costs.

From a valuation perspective, BHP Group Limited (BHP.AX) is currently trading at a P/E ratio of approximately 21.07. The company's balance sheet remains disciplined, with net debt recorded at US$14.7 billion as of 31 December 2025. This results in a gearing ratio of 20.9% and a debt-to-equity ratio of approximately 0.28:1. For income-focused investors, the forward dividend yield stands at approximately 3.8%. The interim dividend for HY26 was declared at US 73 cents per share, representing a 60% payout ratio, consistent with the company's capital allocation framework of returning a minimum of 50% of underlying earnings to shareholders.

Recent Catalysts

The primary catalyst for the recent surge to the 59.78 AUD all-time high is the unprecedented strength in copper prices. As the global energy transition accelerates, the demand for copper in electric vehicle manufacturing and renewable energy grids has created a supply-demand imbalance. BHP Group Limited (BHP.AX) has positioned itself to benefit from this structural deficit through increased production and strategic asset management. Furthermore, the expansion of data centres to support AI technologies has provided a secondary, high-growth demand channel for the metal.

Corporate restructuring and capital recycling have also played a pivotal role in recent months. BHP Group Limited (BHP.AX) announced significant non-core asset monetisations, including a US$4.3 billion silver streaming deal and a US$2 billion agreement regarding its Western Australia Iron Ore power infrastructure. These transactions are designed to unlock up to US$10 billion in capital, which the organisation intends to redeploy into higher-return opportunities or direct shareholder returns. Additionally, the appointment of Brendon Craig as the new chief executive in March 2026 has been viewed by the market as a move toward continuity in the company's long-term decarbonisation and growth strategy.

Technical Analysis

The technical trajectory for BHP Group Limited (BHP.AX) indicates a strong bullish trend, though current levels suggest the stock is reaching an overextended state. The share price of 59.78 AUD is trading significantly above its key moving averages, including the 50-day SMA of 53.6 and the 200-day SMA of 46.78. This positioning confirms a long-term upward bias. The 20-day EMA at 56.1 has acted as a dynamic support level during the recent rally.

However, the RSI (14) has reached 70.77, which is traditionally interpreted as an overbought signal. This suggests that while the momentum is positive, the probability of a short-term consolidation or minor retracement has increased as buyers become exhausted at these record levels. Conversely, the MACD remains bullish, with the MACD line trending above the signal line, indicating that the prevailing trend has not yet shown signs of a definitive reversal.

Analyst Sentiment

Despite the record share price performance, the broader analyst consensus for BHP Group Limited (BHP.AX) remains predominantly 'Neutral' or 'Hold'. This cautious stance is largely attributed to the stock's rapid appreciation, which has pushed it beyond many historical valuation metrics. The average 12-month price target across 16 analysts is 53.153 AUD, which is notably lower than the current trading price of 59.78 AUD. High estimates reach up to 68.09 AUD, while low estimates sit at 39.27 AUD.

Recent rating adjustments reflect this divergence in outlook. CLSA downgraded the stock to 'Hold' on 7 May 2026, citing valuation concerns following the recent rally. In contrast, Goldman Sachs Group recently upgraded BHP Group Limited (BHP.AX) to a 'strong-buy' rating, and JPMorgan maintained a 'Buy' rating in late April 2026. These bullish views are typically predicated on the belief that copper prices will remain elevated for a prolonged period, justifying a higher valuation multiple for the company's shifting earnings base.

Risks and Outlook

The outlook for BHP Group Limited (BHP.AX) is intrinsically tied to global commodity cycles and the pace of the energy transition. While the pivot to copper and potash offers significant growth potential, it also exposes the company to different sets of operational and market risks. A slowdown in global industrial activity or a delay in the rollout of electrification infrastructure could dampen the demand for copper, potentially impacting the company's EBITDA margins. Furthermore, the company's iron ore segment, while highly profitable with low production costs, remains sensitive to the economic health of major importing nations.

Technically, the primary risk is a mean reversion following the overbought RSI (14) reading of 70.77. If the price fails to sustain its position above the 20-day EMA of 56.1, a test of the 50-day SMA at 53.6 could occur. However, the company's strong balance sheet, characterised by a gearing ratio of 20.9%, provides a significant buffer against market volatility and allows for continued investment in the Jansen potash project and other growth initiatives.

BHP Group Limited (BHP.AX) continues to demonstrate operational excellence and strategic foresight in its transition toward a future-facing commodity portfolio. The record share price of reflects the market's recognition of the company's enhanced earnings power in a copper-constrained world. While technical indicators suggest a period of consolidation may be approaching, the underlying financial health—evidenced by a rise in profit and a disciplined debt-to-equity ratio—positions the organisation to maintain its leadership in the global mining sector.

Related Articles

Oil Prices Tumble and Gold Gains as Global Geopolitical Shifts Reshape ASX Outlook

Global market shifts overnight see WTI crude drop 3% and gold futures rise 0.9%, setting up a mixed trading session for ASX energy and gold shares on Friday, June 5, 2026.

Comments

0Loading...

No comments yet. Be the first to share your thoughts.