RBNZ Warns of Slower Recovery Amid Global Energy Disruptions

The Reserve Bank of New Zealand (RBNZ) has released its May 2026 Financial Stability Report, providing a comprehensive assessment of the nation’s financial health against a backdrop of significant global geopolitical tension. Published on May 5, 2026, the report confirms that while the New Zealand financial system remains resilient, the path to economic recovery has become more arduous due to external shocks.

RBNZ Governor Anna Breman, speaking at a media conference on May 6, 2026, highlighted that the ongoing conflict in the Middle East and the subsequent closure of the Strait of Hormuz are exerting considerable pressure on the domestic economy. These events have disrupted global energy markets, leading to a surge in fuel costs that is expected to delay the easing of financial pressures on households and businesses.

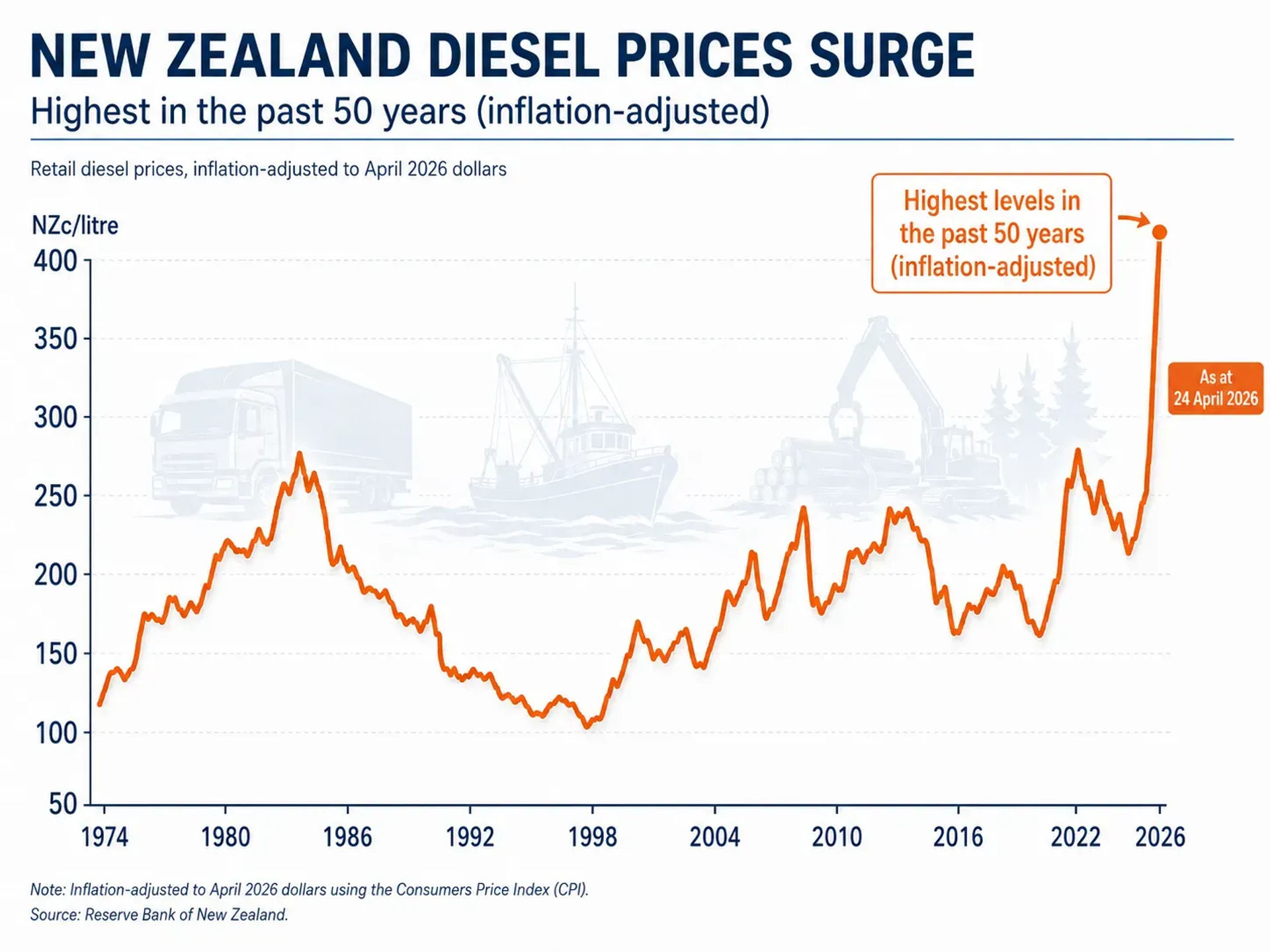

A primary concern identified in the report is the impact of energy prices. Diesel prices, when adjusted for inflation, have reached their highest levels in the past 50 years. This spike is particularly damaging for energy-intensive sectors, including transport, chemical manufacturing, horticulture, forestry, and fishing. The increased cost of production and distribution in these industries is contributing to a broader environment of higher uncertainty and inflation.

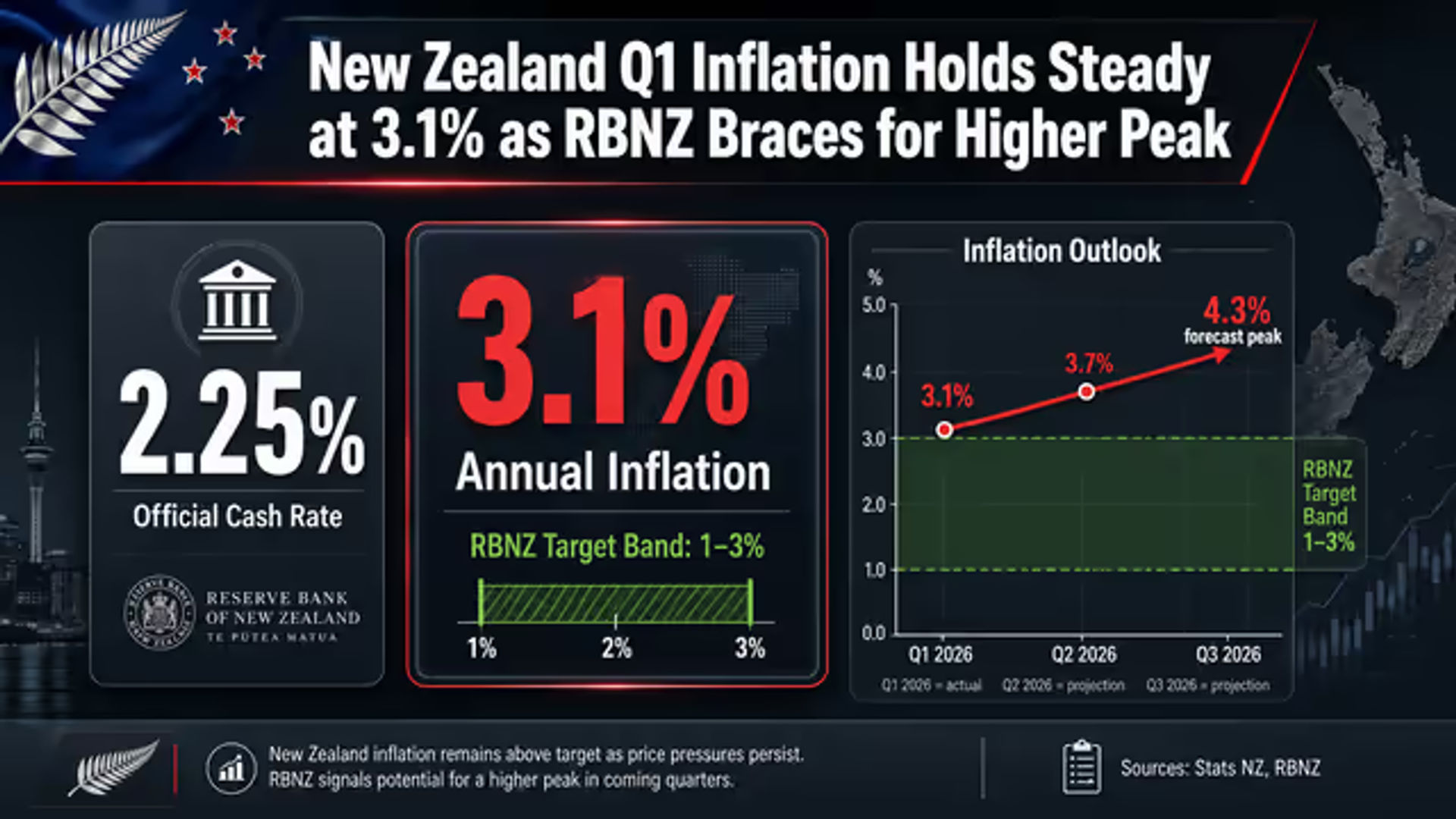

Before the escalation of global conflicts, the New Zealand economy had shown signs of a nascent recovery. However, the RBNZ now expects a slower recovery. Consumer inflation expectations have lifted to 6.6%, a level that mirrors the sentiment seen around 2022 when inflation was at 7%. This persistent inflationary pressure, combined with heightened uncertainty, is likely to weigh on discretionary spending and affect business revenues.

Despite these challenges, the New Zealand banking sector maintains a position of strength. New Zealand banks possess robust capital and funding buffers, which have been bolstered by capital review changes being phased in since last year. Stress tests conducted in 2025 demonstrated that the banking system is capable of withstanding significant economic and geopolitical shocks. Furthermore, a stress test of New Zealand insurers, specifically life and health providers, is progressing throughout 2026 to ensure the broader financial sector remains stable.

Competition within the mortgage market remains visible, with some banks offering mortgage cashback incentives of up to 1.5%. This is a notable increase from the typical 0.9% offers seen previously. It is estimated that these higher cashback offers represent a cost of around $100 million to the banks. While beneficial for some borrowers, the RBNZ notes that rising mortgage rates could still place downward pressure on house prices.

The housing market itself has remained broadly flat for the past three years, following the peak for national house prices in November 2021. Currently, prices remain near the top of the RBNZ’s estimated sustainable range. The combination of high interest rates and a softening labour market suggests that the period of price stability may continue or face further downward adjustments.

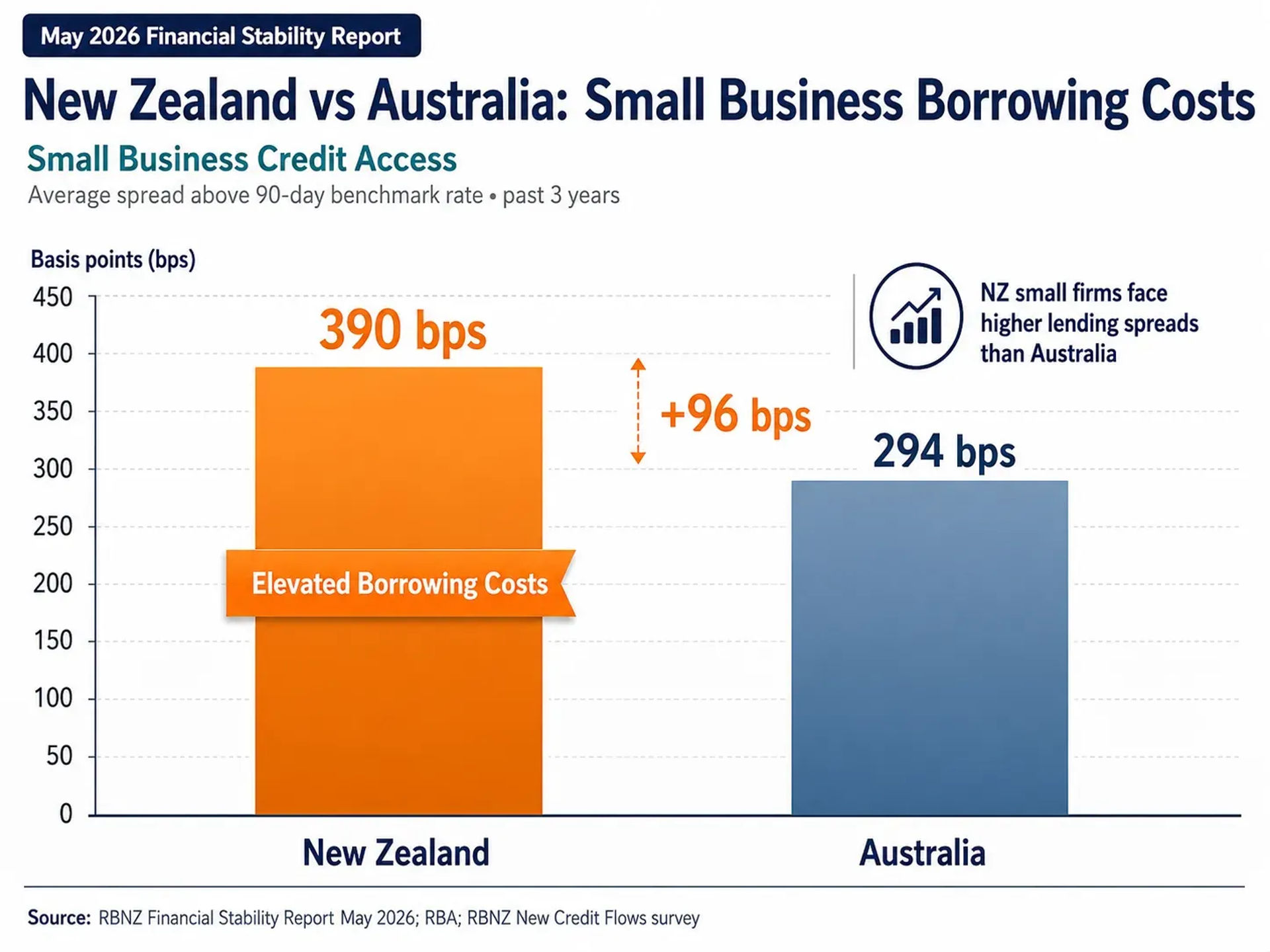

The report also drew attention to the specific difficulties faced by smaller New Zealand businesses. These entities are currently navigating elevated borrowing costs that are, on average, higher than those faced by similar businesses in Australia. This disparity in credit access and cost remains a focal point for the RBNZ, as smaller enterprises are vital to the country's economic fabric but are more vulnerable to rising debt-servicing costs.

Related Articles

Comments

0Loading...

No comments yet. Be the first to share your thoughts.