ASX 200 Snaps Eight-Day Losing Streak as Mining Giants Lead Rebound

The Australian share market found a reprieve on Friday, May 1, 2026, as the S&P/ASX 200 climbed 0.74% to close at 8,729.80 points. The gain effectively ended an eight-session losing streak—the index's longest period of consecutive daily declines since 2018—offering investors a moment of stability following a volatile fortnight of trading.

The recovery was spearheaded by the heavyweight materials sector, which rose 2.09% as bargain hunters returned to the market. Heavyweights BHP Group and Rio Tinto were central to the rebound; BHP shares rose 2.27% to finish the week at A$54.94, while Rio Tinto surged 3.29% to close at A$172.90. This resurgence in the resources sector provided a necessary buffer for the broader index, which had shed approximately 3.5% of its value between April 17 and April 30.

Manufacturing Data and Bargain Hunting

Market sentiment was further bolstered by positive manufacturing data from both China and Australia. The S&P Global Australia Manufacturing PMI returned to expansionary territory in April, climbing to 51.3 from 49.8 in March. This shift indicates a modest improvement in domestic industrial health, though manufacturers continue to report significant headwinds from surging input costs, particularly fuel and logistics expenses.

Simultaneously, stronger-than-expected industrial data from China provided a tailwind for Australia’s iron ore exporters. Analysts noted that the combination of oversold conditions and fundamental support from the manufacturing sector encouraged institutional buyers to step back into the market on Friday.

The Inflationary Backdrop

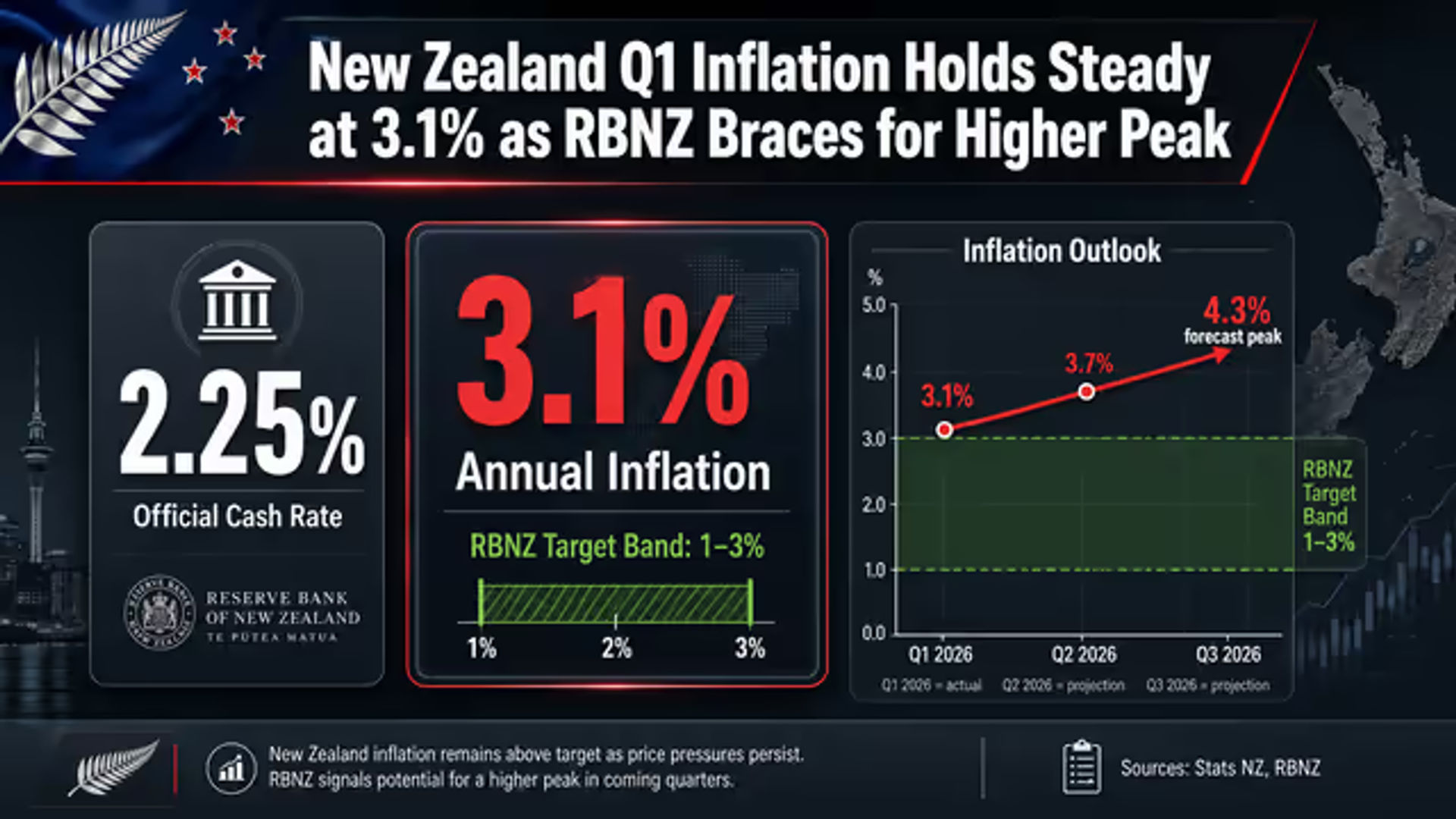

Despite the positive close on Friday, the underlying economic landscape remains challenging for both the Australian and New Zealand economies. Australia’s headline inflation accelerated sharply to 4.6% in March 2026, up from 3.7% previously. This figure remains significantly above the Reserve Bank of Australia’s (RBA) target band of 2–3%.

Underlying inflation, measured by the trimmed mean, stood at 3.5% for the year to March 2026. This persistent price pressure has been exacerbated by global energy costs. In late April, Brent crude oil prices surged above US$120 a barrel as geopolitical tensions in the Middle East escalated, creating renewed disruption concerns around the Strait of Hormuz. Adding a new layer of complexity to global energy markets, the United Arab Emirates (UAE) announced its withdrawal from OPEC and OPEC+ on May 1, a move that could have long-term implications for global supply stability.

RBA Rate Hike Expectations

With inflation proving stickier than anticipated, market attention is now firmly fixed on the RBA board meeting scheduled for Tuesday, May 6, 2026. Financial markets are currently pricing in an approximately 70-80% probability of a 25 basis point increase to the cash rate.

Related Articles

Comments

0Loading...

No comments yet. Be the first to share your thoughts.