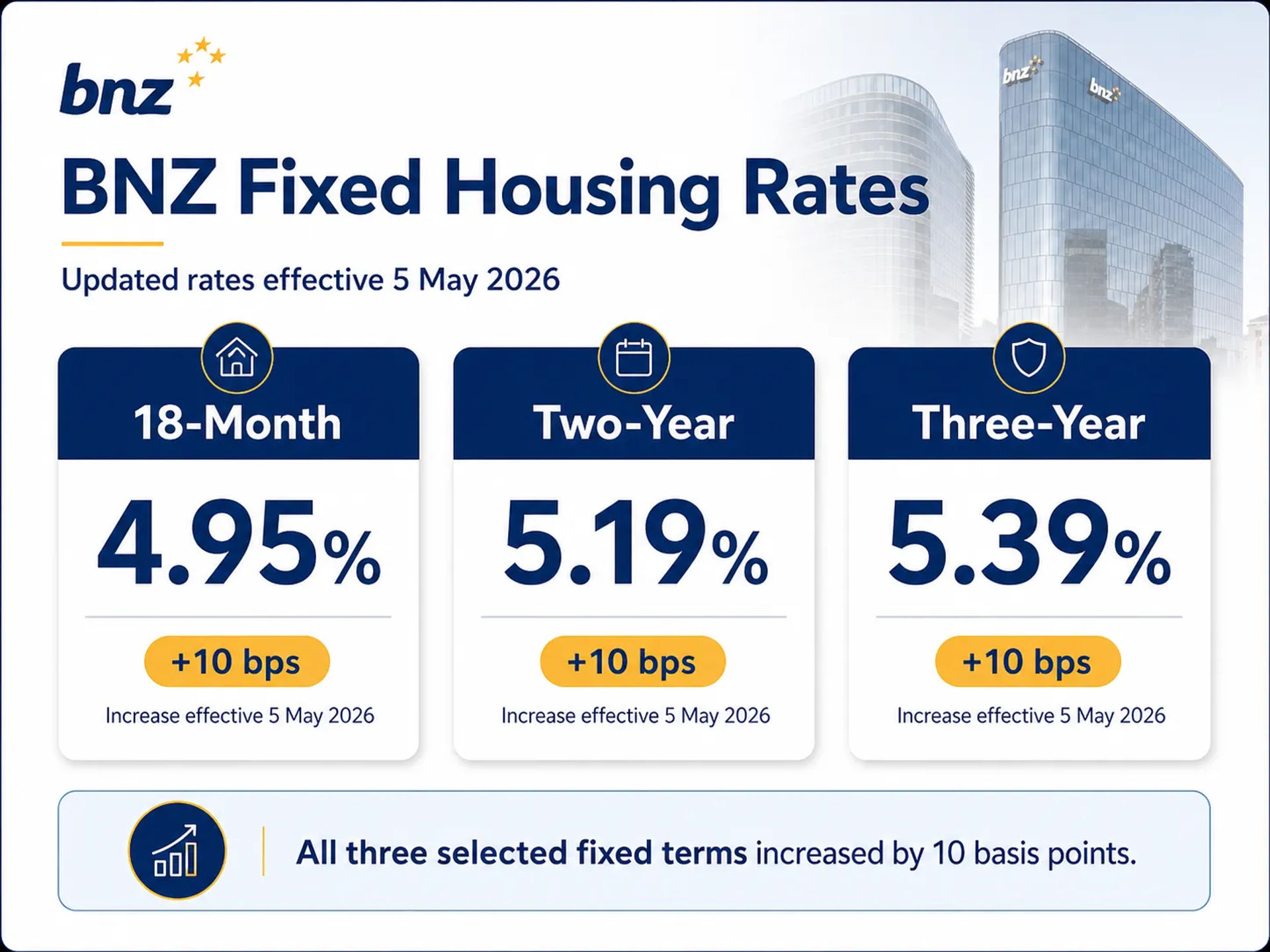

Bank of New Zealand Increases Fixed Housing Interest Rates Effective Today

Bank of New Zealand has implemented a series of increases to its fixed housing interest rates, effective Tuesday, May 5, 2026. The adjustments see several key terms rise by 10 basis points, reflecting ongoing pressure from wholesale markets and global economic conditions. This move marks the second time in less than a fortnight that the lender has adjusted its pricing for home loans, signalling a period of heightened activity in the mortgage market.

The 18-month fixed housing interest rate has moved to 4.95%. For those looking at longer-term stability, the two-year fixed housing interest rate is now 5.19%, while the three-year fixed housing interest rate has reached 5.39%. These changes represent a consistent upward trend in lending costs for New Zealand homeowners and investors alike. The 10 basis points increase across these three durations suggests a broad-based adjustment to the organisation's funding outlook.

This latest move follows a previous round of adjustments made by Bank of New Zealand on April 23, 2026. During that earlier shift, the bank lifted several rates, including the 18-month and two-year terms. The frequency of these adjustments—twice within a two-week period—highlights the volatility currently present in the financial sector and the speed at which wholesale market changes are being passed through to retail customers.

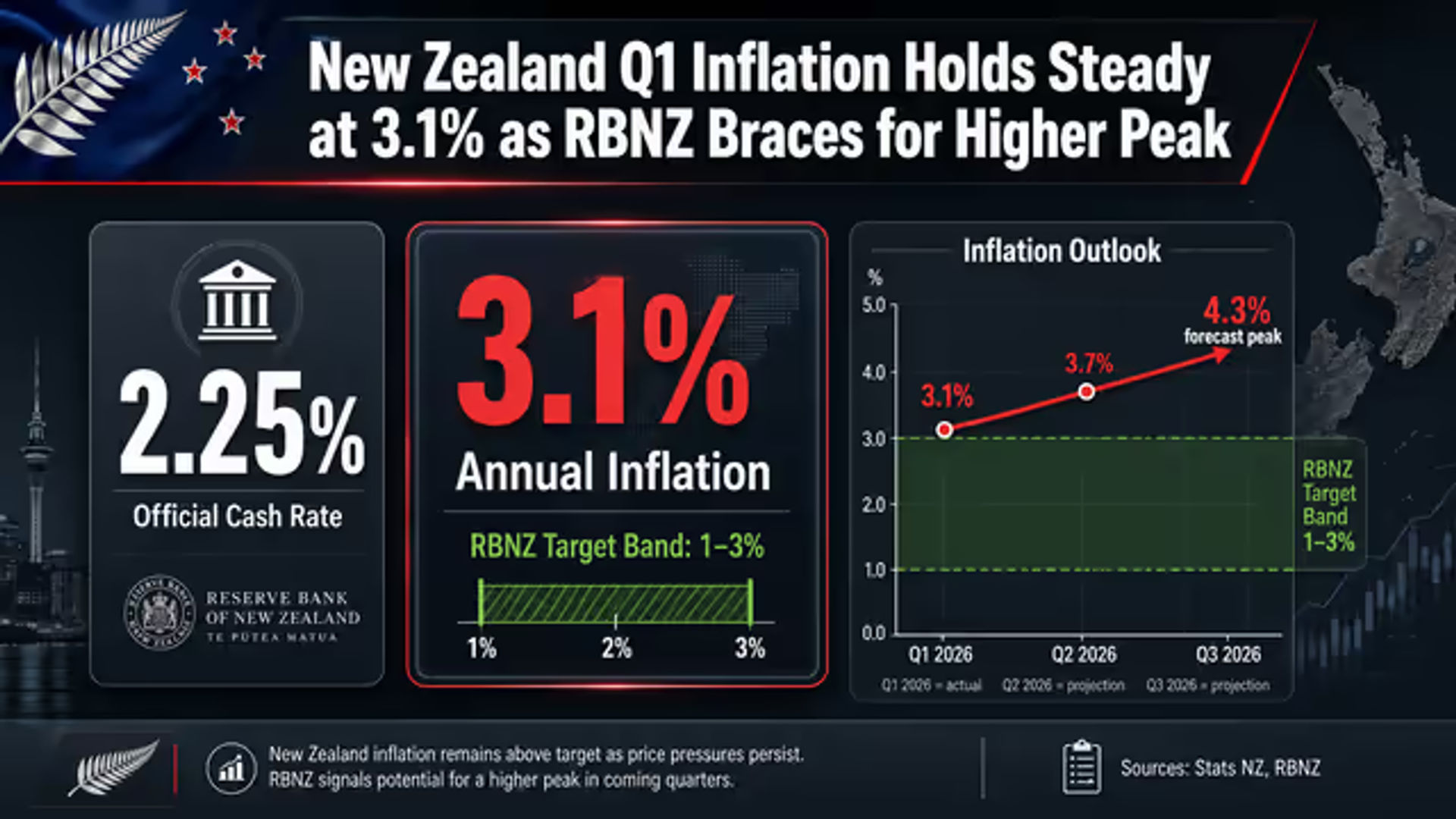

The upward movement in retail rates comes despite the Reserve Bank of New Zealand maintaining a steady hand on the Official Cash Rate. At its April 2026 meeting, specifically on April 8, 2026, the central bank held the Official Cash Rate at 2.25%. While the benchmark rate remained unchanged, the Reserve Bank of New Zealand noted concerns regarding global inflationary pressures. The next Official Cash Rate decision and Monetary Policy Statement are scheduled for May 27, 2026, a date that market participants are watching closely for signals of future policy direction.

External factors are playing a significant role in the pricing of New Zealand mortgages. Wholesale interest rates have been climbing, driven in part by an ongoing oil crisis linked to conflict in the Middle East. This geopolitical instability has contributed to global inflationary pressures, which filter through to the costs banks face when securing funding for their lending portfolios. The impact of these global events is being felt directly by New Zealand borrowers as banks adjust their margins to account for higher costs in the international money markets.

In addition to the rate changes, Bank of New Zealand recently disclosed its financial performance for the half-year ending March 31, 2026. The organisation recorded a statutory net profit of $494 million. This figure represents a 37.9% decrease compared to the same period in the previous year. The decline in profitability occurs as the banking sector navigates a complex environment of rising costs, shifting consumer demand, and a cooling housing market. The 37.9% drop in profit highlights the challenges faced by large financial institutions in the current economic climate.

For mortgage holders and prospective buyers, these increases mean higher debt-servicing costs. While the Reserve Bank of New Zealand has kept the Official Cash Rate at 2.25% for now, the bank-led increases suggest that the cost of borrowing is rising independently of immediate central bank action. Other major institutions, including ASB, Westpac, ANZ, Kiwibank, and TSB, continue to monitor the market as these wholesale pressures persist. The 3.1% figure associated with market indicators further underscores the inflationary environment that lenders are currently managing.

Related Articles

Comments

0Loading...

No comments yet. Be the first to share your thoughts.