Bank of New Zealand statutory net profit falls 37.9 per cent following software policy change

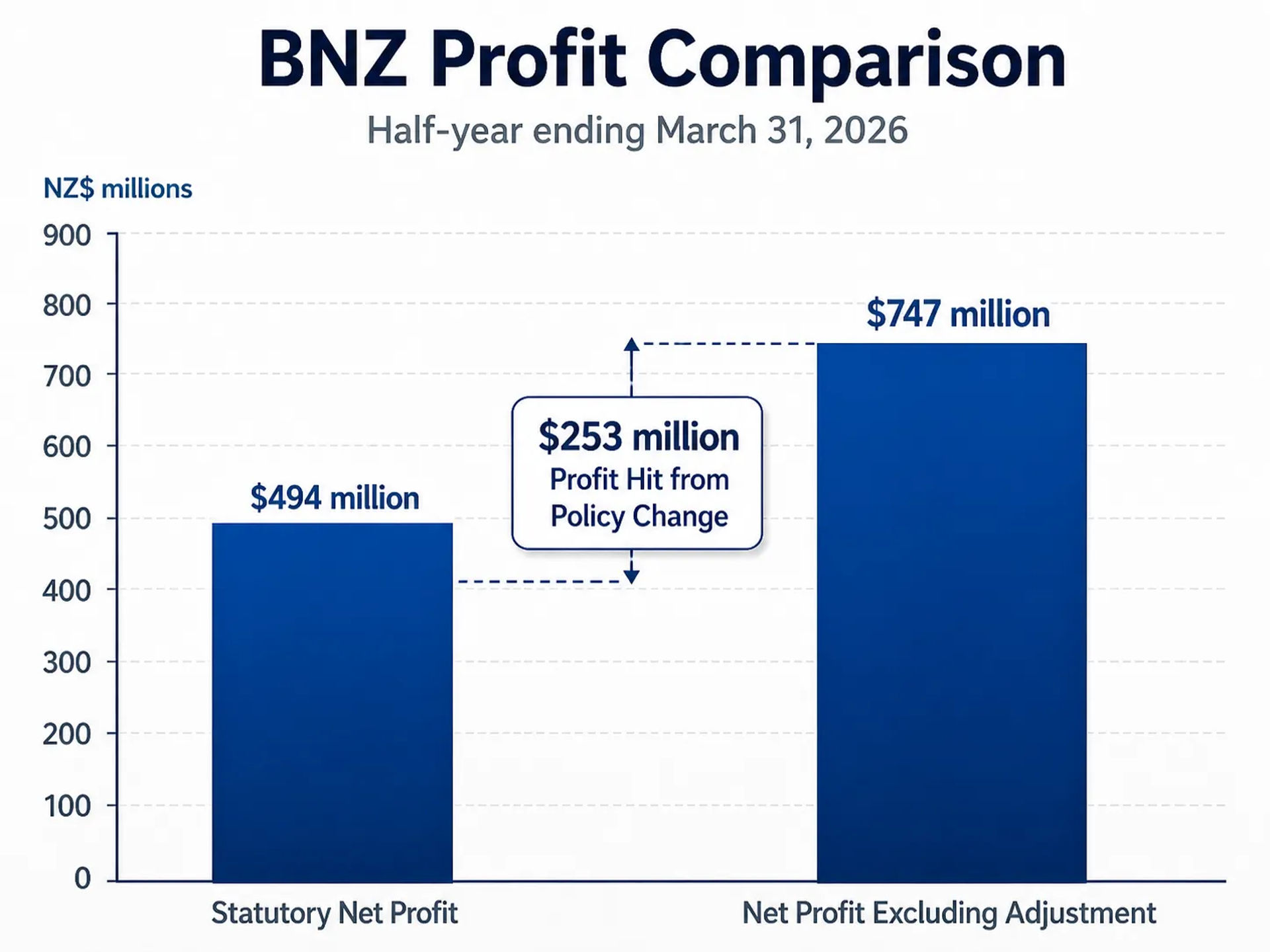

Bank of New Zealand (BNZ) has reported a statutory net profit of $494 million for the half-year ending March 31, 2026. This result represents a significant decrease of 37.9 per cent, or $301 million, compared to the same period in the previous year. The primary driver behind this substantial decline in reported profit was a one-off, post-tax reduction of $253 million in capitalised software assets. This reduction followed a strategic change in accounting policy designed to address the rapid obsolescence of technology and the accelerating adoption of Artificial Intelligence (AI) within the banking sector.

The accounting policy change resulted in a $352 million reduction in the capitalised software balance as of March 31, 2026. This adjustment aligns the organisation's financial reporting with its parent company, National Australia Bank Group (NAB). The decision to shorten the useful life of software assets reflects a global environment where technological advancements are occurring at an unprecedented pace, necessitating a more conservative approach to how these digital assets are valued on the balance sheet.

When excluding the impact of this one-off accounting adjustment, the underlying financial performance of the bank remained relatively stable. The net profit excluding the adjustment was $747 million, which represents a more modest decline of $48 million from the prior period. Total revenue for the half-year reached $1,760 million, marking a slight increase of 0.7 per cent. Operating expenses, when excluding the software adjustment, rose by 4.3 per cent to $701 million, reflecting ongoing investment in the business and inflationary pressures.

Despite the impact of the accounting change on the headline profit figure, the bank experienced growth across its core lending portfolios. Total lending increased by $5.1 billion, or 4.7 per cent, to reach a total of $113.6 billion. This growth was supported by a 6.6 per cent increase in home lending and a 2.2 per cent rise in business lending. Customer deposits also saw an upward trend, increasing by $4.5 billion, or 5.3 per cent, during the half-year period.

Net interest margin (NIM) experienced a slight compression, decreasing by 4 basis points. This decline was attributed to intense market competition for customers in both the lending and deposit sectors. The competitive environment has required the bank to balance volume growth with margin preservation as customers seek the best available rates in a shifting economic landscape.

Credit impairment provisioning for the period ending March 31, 2026, totalled $995 million. This represents a year-on-year increase of $20 million in total credit impairment provisioning. The bank has maintained a cautious approach to its provisioning levels, taking into account potential economic headwinds and external factors, including the ongoing conflict in the Middle East, which has influenced the broader economic outlook. These provisions are designed to ensure the organisation remains resilient against potential future credit losses.

Related Articles

Comments

0Loading...

No comments yet. Be the first to share your thoughts.