National Australia Bank Reports A$2.75 Billion Half-Year Profit Amid Software Charges and Economic Volatility

National Australia Bank (NAB) has announced its financial results for the first half of the 2026 fiscal year, reporting a statutory net profit of A$2.75 billion for the six-month period ending March 31, 2026. This figure represents a 19.3% decline compared to the same period in the previous year. The result fell short of average analyst expectations, which had been positioned at A$3 billion by Bloomberg and between A$2.93 billion and A$2.95 billion according to Visible Alpha estimates.

The decline in statutory profit was largely driven by a significant non-cash item related to the bank's internal accounting. NAB recognised a A$949 million post-tax charge, which equates to A$1.35 billion on a pre-tax basis, following a change in its software capitalisation policy. This accelerated amortisation charge reflects a shift in how the organisation manages its technology investments. When excluding this large notable item, the bank's cash earnings reached A$3.588 billion, an increase of 2.3% compared to the second half of the 2025 financial year. The reported cash earnings for the period stood at A$2.64 billion.

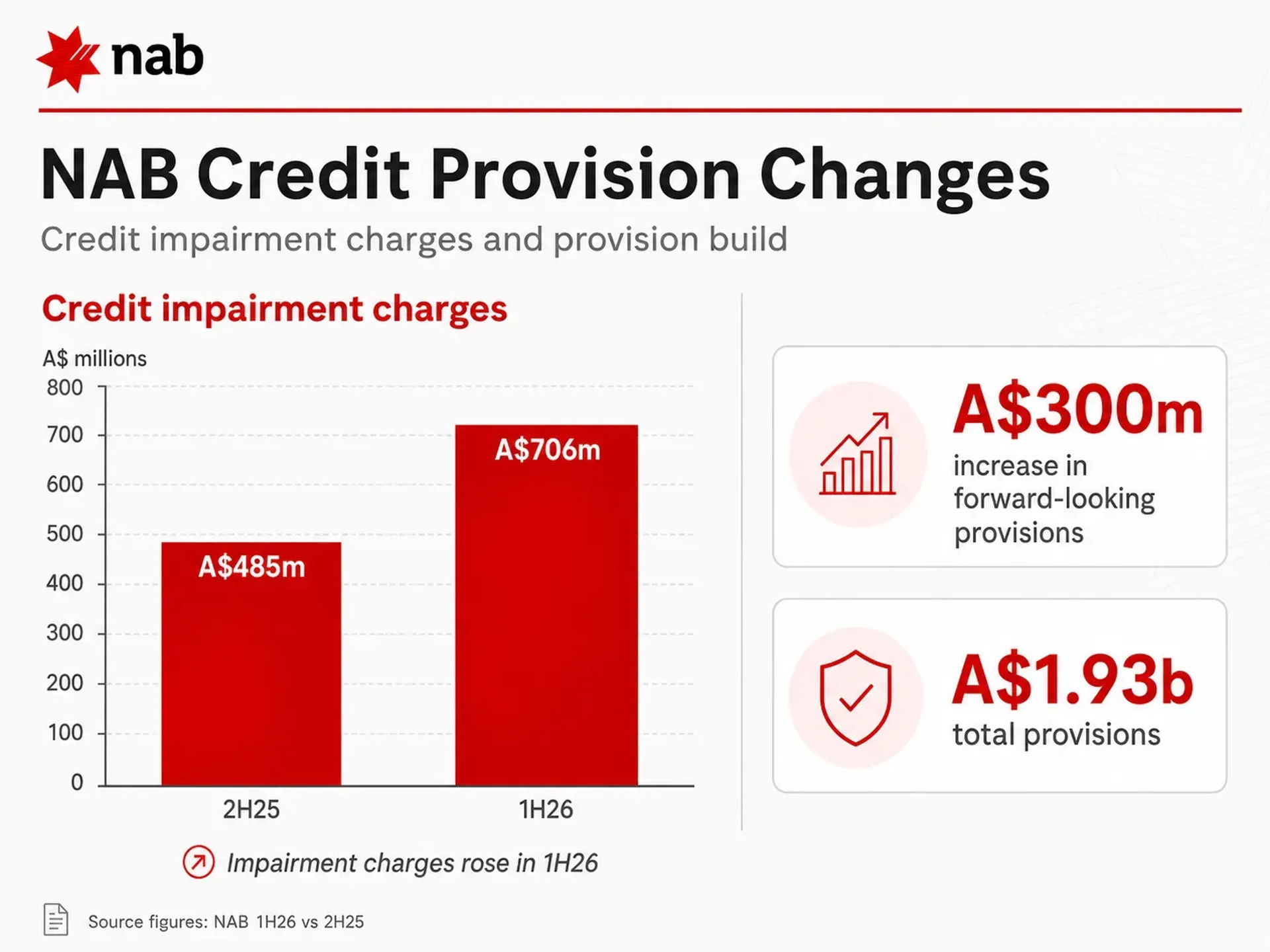

Credit Impairment and Economic Provisions

Financial performance for the half-year was also influenced by an increase in credit impairment charges, which rose to A$706 million. This is a notable increase from the A$485 million recorded in the second half of 2025. As part of its risk management strategy, NAB increased its forward-looking collective provisions by A$300 million, bringing the total forward-looking collective provisions to A$1.93 billion as of March 31, 2026.

This decision to bolster provisions follows an announcement on April 19, 2026, where the bank flagged higher charges in response to a deteriorating economic outlook. The bank has identified increased macroeconomic uncertainty, specifically citing geopolitical tensions in the Middle East, as a primary driver for this cautious stance. These global factors are expected to contribute to higher fuel costs, supply chain disruptions, and persistent inflationary pressures, which may impact the broader business environment in Australia and New Zealand.

Lending Growth and Margins

Despite the statutory profit decline, NAB experienced growth across its lending portfolios. Gross loans and advances increased by 2.9% over the half-year period. When adjusted for the impact of New Zealand dollar translation, this growth rate was 3.7%. The Business & Private Banking division was a particular area of strength, recording lending growth of 5.4%.

The bank's net interest margin, a key measure of profitability in lending, stood at 1.81% for the half-year. This represents an increase of 3 basis points, reflecting the bank's ability to manage its margins in a complex interest rate environment. This follows the February 18, 2026, First Quarter Trading Update, which had previously noted an improvement in asset quality despite rising personnel and technology costs.

Shareholder Returns and Capital Management

NAB has declared a fully franked interim dividend of 85 Australian cents per share, maintaining the same level as the prior period. The ex-dividend date for this payment is set for May 7, 2026, with the record date following on May 8, 2026. Shareholders have until May 11, 2026, to make elections regarding the Dividend Reinvestment Plan (DRP). The interim dividend is scheduled for payment on July 2, 2026.

Related Articles

Comments

0Loading...

No comments yet. Be the first to share your thoughts.