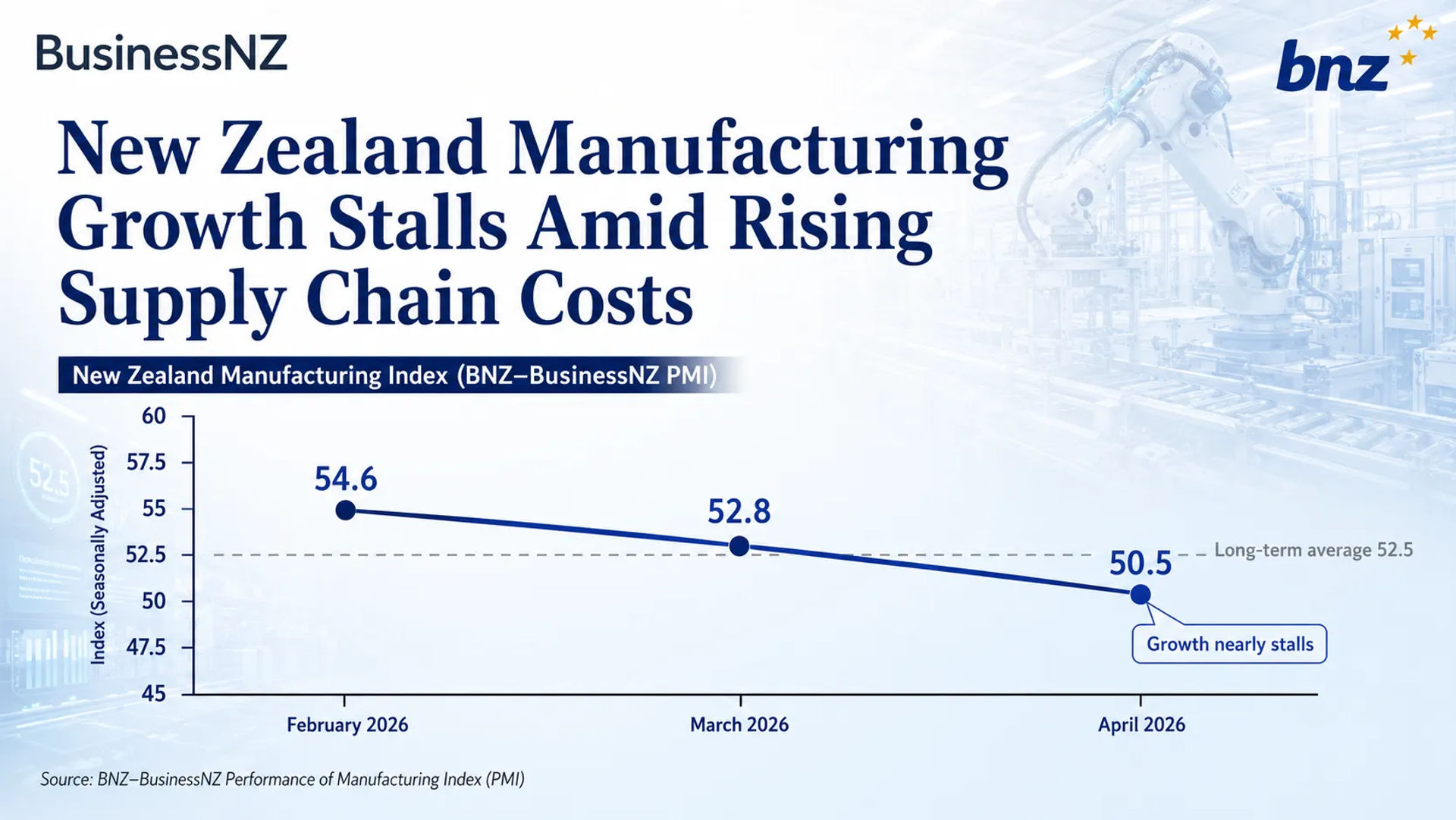

New Zealand Manufacturing Growth Stalls Amid Rising Supply Chain Costs

New Zealand's manufacturing sector experienced a sharp deceleration in April 2026, with the New Zealand Performance of Manufacturing Index (PMI) falling to 50.5. This figure represents a significant drop from the revised 52.8 recorded in March 2026 and the 54.6 seen in February 2026. While a reading above 50.0 technically indicates the sector remains in expansion, the current level sits well below the NZ PMI long-term average of 52.5, marking the lowest point for industrial activity in six months.

The headline figure masks deeper concerns within the sub-indexes, particularly those that signal future production pipelines. Forward-looking indicators have moved into contractionary territory, suggesting that the sector's earlier resilience is beginning to fade. The month of April represents a potential turning point for the broader economy, as the sustained pressure on global logistics begins to manifest in domestic output data.

Contraction in Forward Indicators and Supply Chains

The most significant downward pressure in the April data came from a contraction in new business and the delivery of essential components. The New Orders sub-index fell to 48.2 in April 2026, marking a shift away from the growth seen earlier in the year. Simultaneously, the Raw Material Deliveries sub-index plummeted to 46.5. This is the lowest level recorded for raw material deliveries since July 2024, highlighting the severity of the current logistical bottlenecks.

These disruptions are directly linked to the ongoing conflict in the Middle East, which has fundamentally altered international shipping routes and cost structures. Approximately 63.6% of businesses surveyed in April 2026 cited negative influences on their operations, an increase from the 62.0% reported in March 2026. The primary concerns for these organisations include:

- Escalating international freight costs and surcharges

- Significant delays in the arrival of raw materials and intermediate goods

- Rising fuel prices impacting domestic distribution networks

- General uncertainty regarding the duration of the Middle East conflict

Divergence Across Firm Sizes

The impact of the slowdown is not being felt uniformly across the industry. There is a stark divergence between small-scale operators and larger industrial organisations. Micro-firms, defined as those with 1-10 employees, are facing the most acute pressure, recording a sub-index of 39.2 in April 2026. This indicates a firm contraction for the smallest players in the New Zealand manufacturing landscape.

Related Articles

Comments

0Loading...

No comments yet. Be the first to share your thoughts.