NZ Property Values Edge Up Slightly in April, but Auckland and Wellington Decline Amid Sluggish Outlook

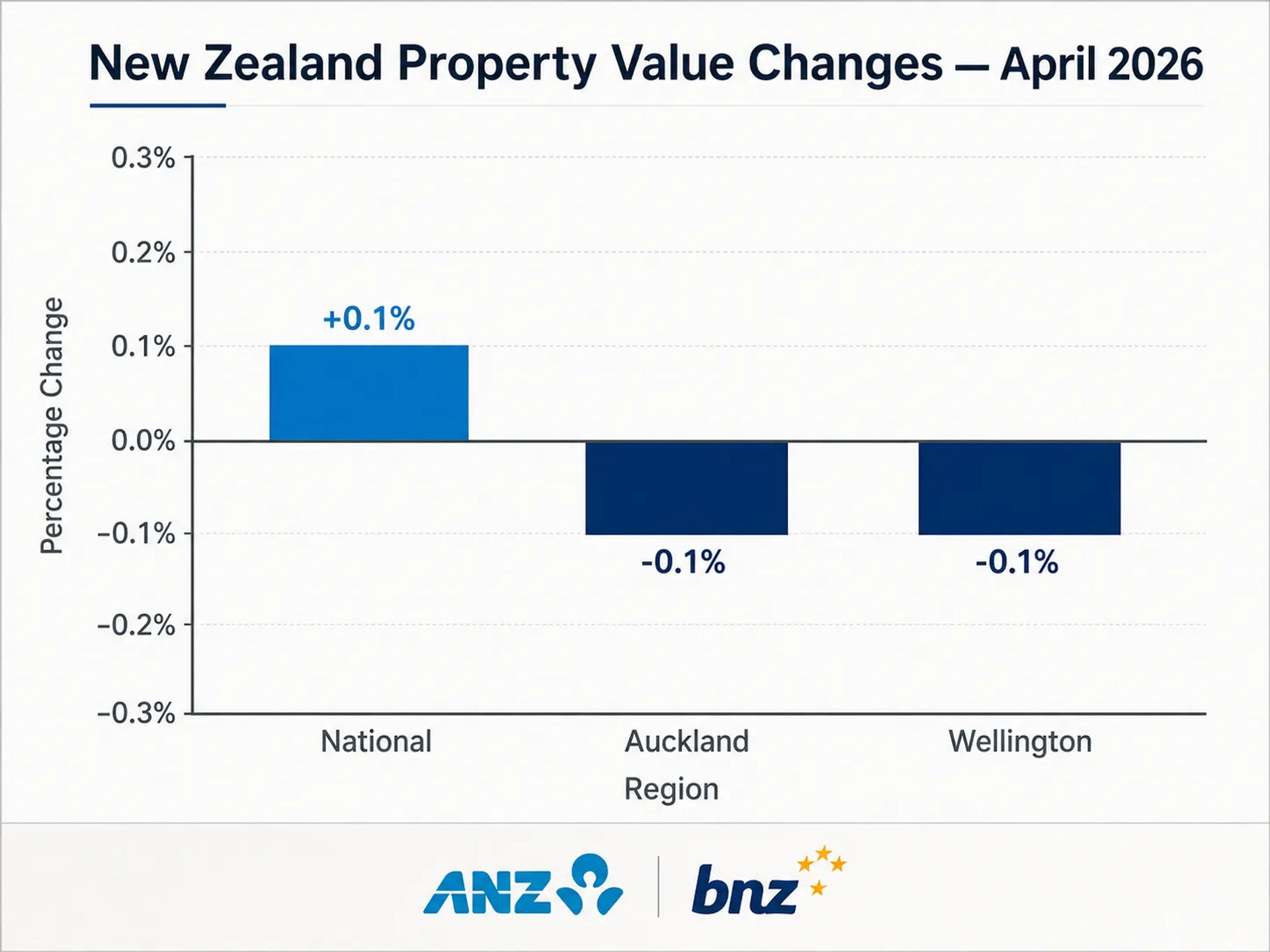

New Zealand’s residential property market continued its modest recovery in April 2026, though a widening gap between regional performance and major urban centres suggests a period of prolonged stagnation ahead. According to the latest data from Cotality, the national median residential property value rose by 0.1% in April, reaching $809,101. This marks the third consecutive month of incremental gains for the national index, following a 0.6% rise in February and a 0.2% increase in March.

Despite the national uptick, the country’s two largest property markets—Auckland and Wellington—showed signs of renewed weakness. Both cities recorded a 0.1% decline in median values over the month of April. Auckland’s median property value now sits at just over $1.04 million, while Wellington’s median value has dipped to $780,504. The figures underscore a 'two-speed' market where regional resilience is being offset by affordability constraints and high listing volumes in the main metropolitan hubs.

The Urban Correction Continues

The April data highlights the significant distance the major centres remain from their historical peaks. Auckland property values are now down 3% over the last year and remain 22.9% below their post-pandemic highs. The situation in Wellington is even more pronounced; while values fell only 1.1% over the past 12 months, the capital’s median value is currently 25% lower than its previous peak.

Analysts note that the sluggish performance in these cities is largely a product of high inventory levels. With more choices available to buyers and sales volumes remaining historically low, the urgency that typically drives price growth in Auckland and Wellington is absent. For many existing homeowners in these regions, the reality of stagnant or declining equity is compounded by the rising cost of debt servicing.

RBNZ Hawkishness and the Mortgage Squeeze

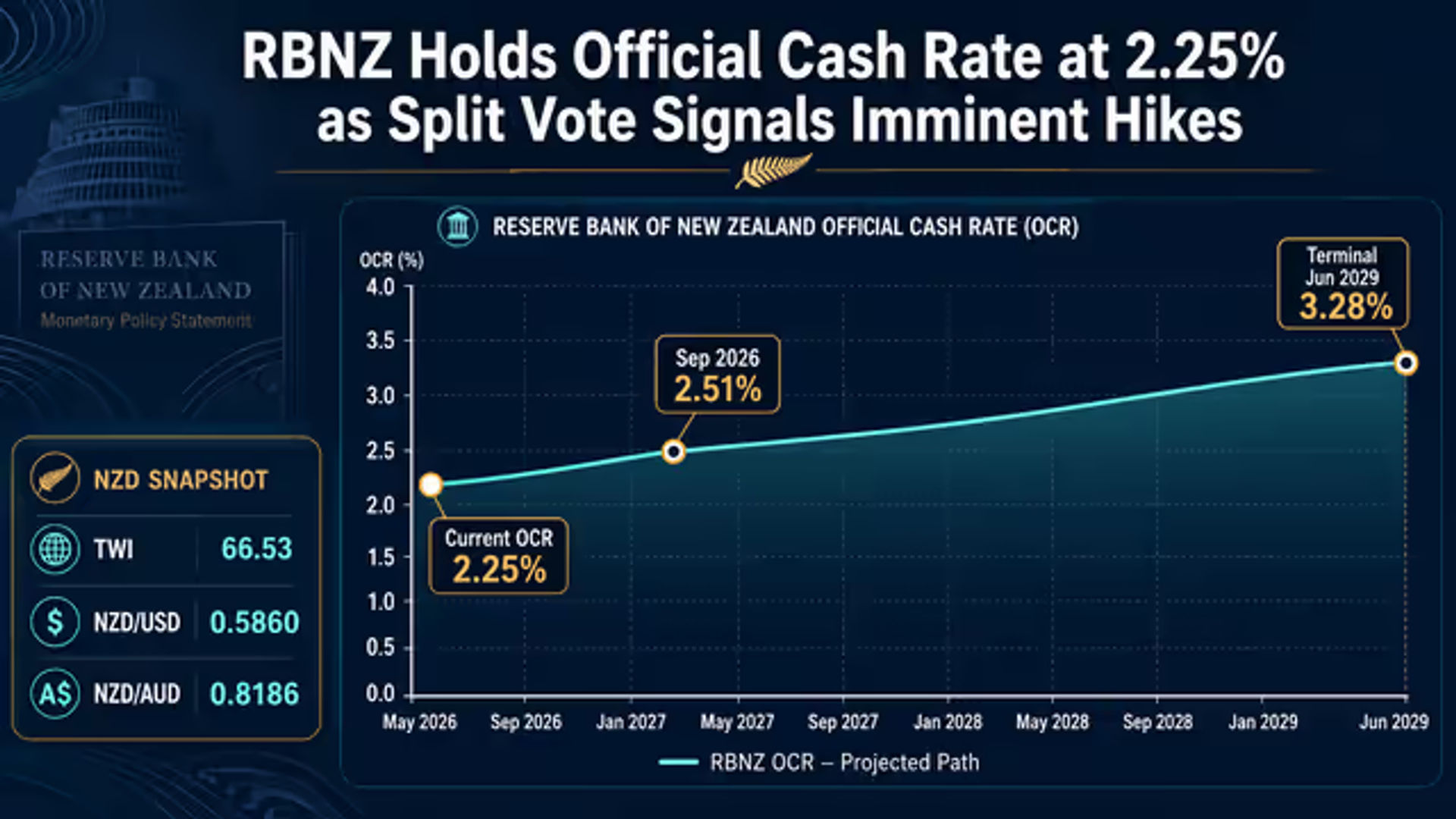

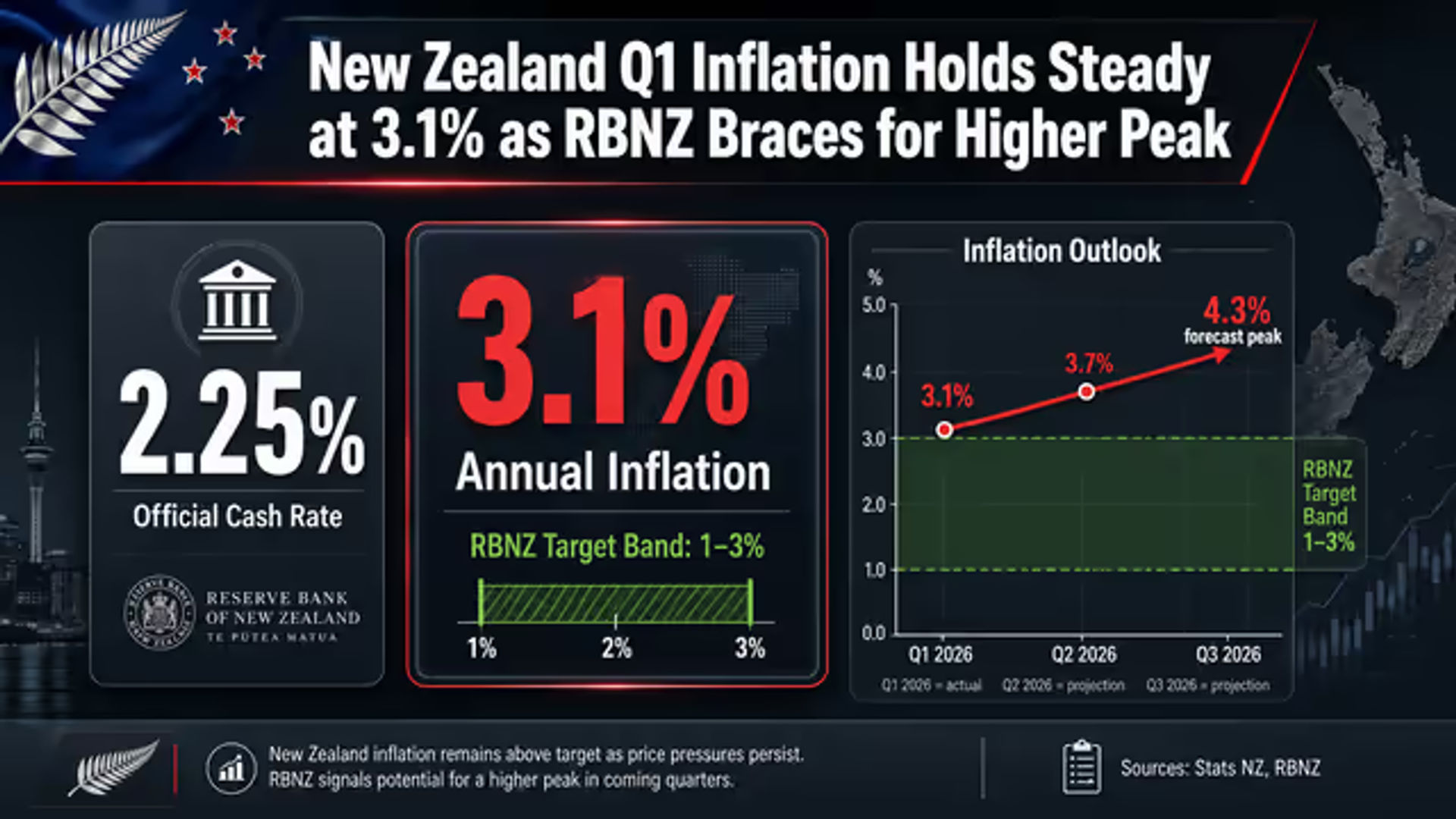

Central to the market’s cautious sentiment is the Reserve Bank of New Zealand’s (RBNZ) current monetary policy trajectory. In April 2026, the RBNZ held the Official Cash Rate (OCR) steady at 2.25%. However, the central bank adopted what economists describe as a 'hawkish hold,' signaling that future hikes remain a possibility if inflation does not retreat toward the 1% to 3% target range. Inflation is currently forecast to hit 4.2% in the second quarter of 2026.

This stance has immediate implications for mortgage holders. While some fixed-term rates had stabilised earlier in the year, several lenders have recently begun nudging rates upward in response to the RBNZ’s rhetoric. Current market forecasts suggest that mortgage rates will likely fluctuate between 4.75% and 5.50% over the next 12 to 24 months.

For first-home buyers, this creates a paradoxical environment. While the softening prices in Auckland and Wellington offer a lower entry point than in previous years, the cost of borrowing remains a significant barrier. The reduction in competition from investors—who are also grappling with higher interest costs and economic uncertainty—has provided some breathing room for owner-occupiers, yet the 'mortgage squeeze' continues to limit overall purchasing power.

Related Articles

Comments

0Loading...

No comments yet. Be the first to share your thoughts.