Geopolitical Shock Sends New Zealand Business Confidence Into Negative Territory

New Zealand business confidence has experienced a sharp reversal, with the headline ANZ Business Outlook Index plummeting to -10.6 in April 2026. This marks the first negative reading for the index since August 2023 and represents a significant 43-point swing from the +32.5 recorded in March 2026.

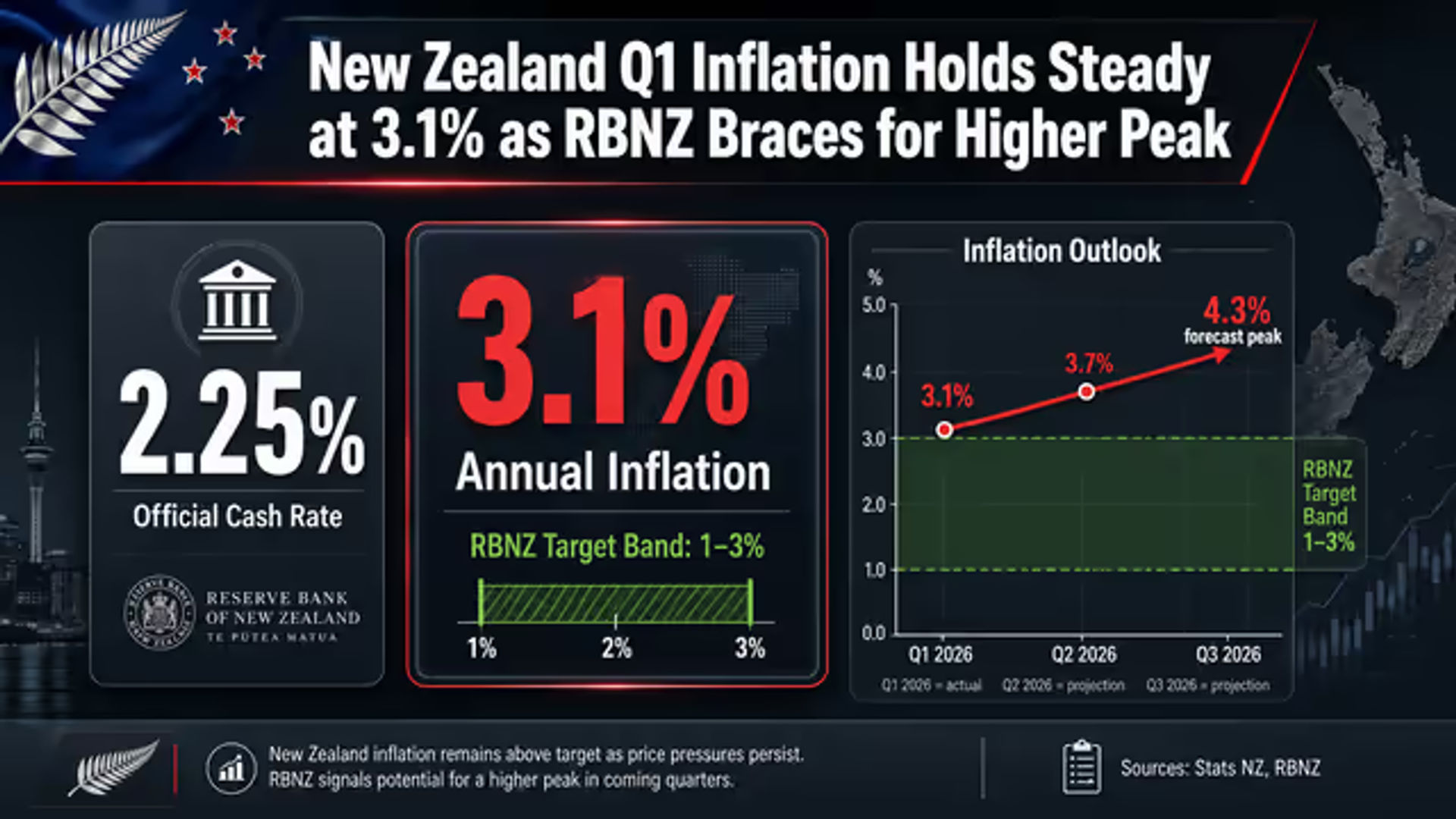

The rapid deterioration in sentiment is primarily attributed to the escalating conflict in the Middle East, specifically the US-Israel war on Iran and the subsequent disruption of the Strait of Hormuz. These external shocks have triggered a substantial cost surge for New Zealand firms, complicating the path forward for the Reserve Bank of New Zealand (RBNZ) as it navigates a landscape of rising inflation expectations and weakening growth.

A Broad-Based Decline in Activity

The April survey results indicate that the negative sentiment is not isolated to a single sector but is instead reflected across almost every key economic indicator. The 'own activity' outlook, which often serves as a more reliable gauge of actual economic performance than the headline confidence figure, dropped from 39.3 in March to 19.6 in April. While still in positive territory, the momentum has clearly stalled, with the retail sector emerging as the weakest link, recording a flat reading of zero.

Export intentions also saw a dramatic decline, falling from 15.2 to 1.1. This suggests that New Zealand’s primary producers and manufacturers are bracing for a significant slowdown in global demand and logistics hurdles. The most striking figure, however, was found in profit expectations, which swung from +19.7 in March to -13.3 in April. The agriculture sector reported the most pessimistic outlook for profitability, reaching a low of -40.

Investment and employment intentions followed a similar downward trajectory. Investment intentions fell from 14.5 to 3.3, while employment intentions turned negative for the first time since mid-2024, dropping from +9.4 to -2.7. This shift suggests that firms are moving into a defensive posture, prioritizing cost containment over expansion as uncertainty regarding fuel supplies and global trade routes persists.

Geopolitical Shocks and the Cost Inflation Dilemma

The timeline of the decline correlates directly with the heightening of geopolitical tensions. On March 1, 2026, Prime Minister Christopher Luxon and Foreign Minister Winston Peters issued a joint statement regarding the Middle East conflict, and by March 21, New Zealand had joined 19 other nations in condemning the closure of the Strait of Hormuz.

By late March, the impact was already being felt in the data. ANZ noted that survey responses collected after the initial geopolitical shock averaged -22.5, suggesting the final April headline of -10.6 may actually reflect a slight stabilization after an initial period of high volatility. However, the underlying cost pressures remain severe. Cost expectations for the next three months surged to 4.57% from 2.99%, the highest reading since May 2023.

Simultaneously, one-year inflation expectations rose to 3.81% from 3.08%, marking the highest level since February 2024. This presents a difficult scenario for the RBNZ. On March 24, the central bank acknowledged that the conflict would likely result in higher near-term inflation and weaker growth. Treasury scenarios released the same month forecasted a worst-case inflation scenario of 7.4% if energy supply disruptions were prolonged.

Related Articles

Comments

0Loading...

No comments yet. Be the first to share your thoughts.