RBNZ Holds OCR at 2.25% as Global Geopolitics Reignite Inflation Fears

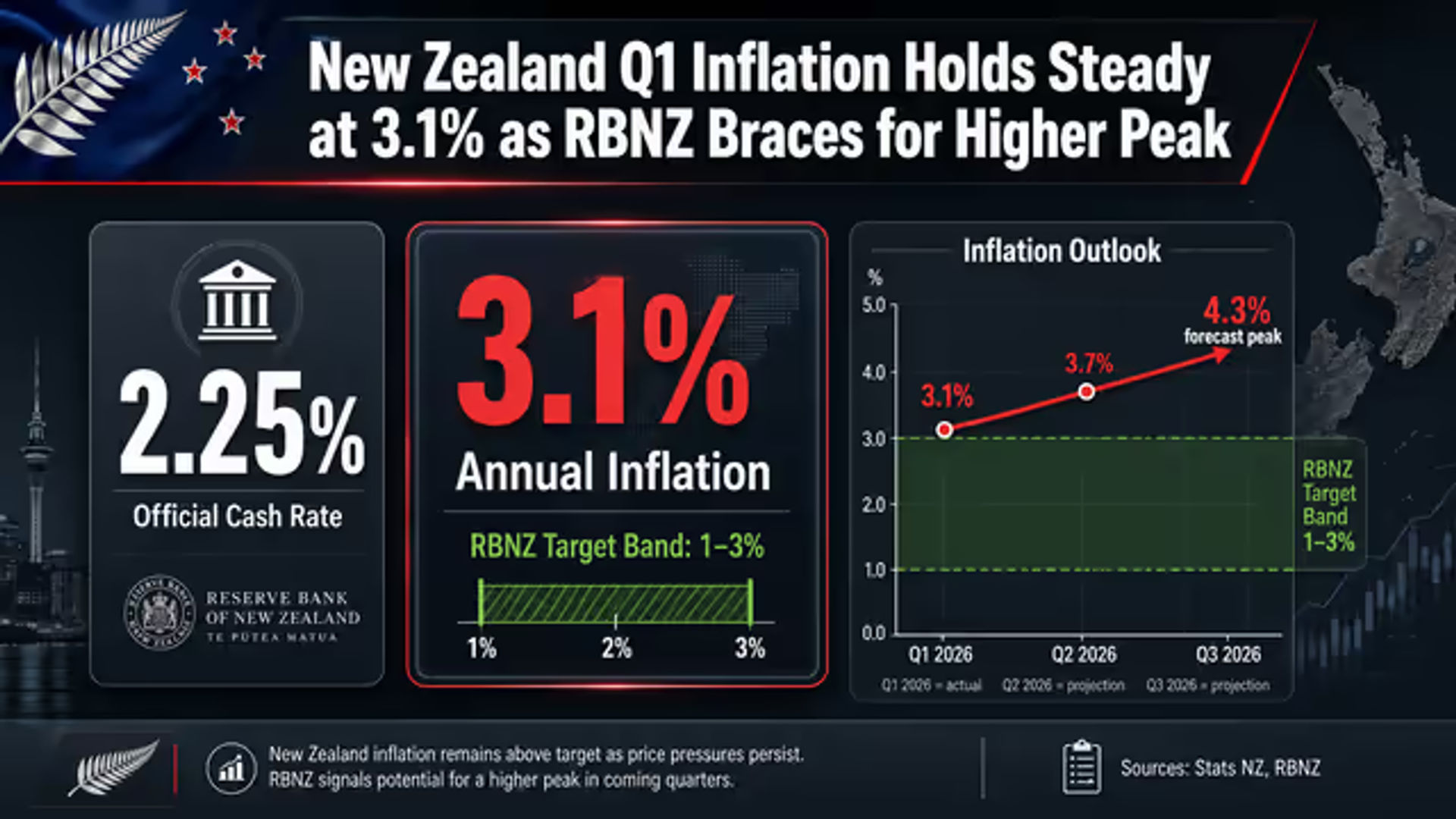

The Reserve Bank of New Zealand (RBNZ) has maintained the Official Cash Rate (OCR) at 2.25% following its April 8, 2026, policy review. The decision, reached by consensus of the Monetary Policy Committee (MPC), signals a cautious pause in the easing cycle as persistent domestic price pressures and volatile global commodity markets threaten to push inflation further away from the bank’s 2% midpoint target.

While the RBNZ had aggressively reduced the OCR from a peak of 5.25% in August 2024 to its current level by November 2025, the disinflationary momentum appears to have stalled. Fresh data released on April 21 shows New Zealand’s annual Consumer Price Index (CPI) remained at 3.1% in the first quarter of 2026, unchanged from the final quarter of 2025 and exceeding market expectations of 2.9%.

Inflation Drivers: A Double-Edged Sword

The persistence of inflation is being driven by a combination of domestic structural costs and external shocks. According to the RBNZ, non-tradeable (domestic) inflation rose by 3.5% annually in Q1 2026. A primary culprit in this category was electricity prices, which surged by a staggering 12.5% year-over-year, placing significant strain on both household budgets and industrial margins.

On the tradeable side, which saw a 2.5% increase, the impact of global instability is becoming increasingly visible. Petrol prices emerged as the dominant quarterly driver, rising 3.5% in the first three months of the year. While prices showed signs of easing in January and February, they climbed sharply in March as the conflict in the Middle East began to weigh more heavily on global oil and refined petroleum markets.

In its April statement, the RBNZ noted significant concerns regarding "second-round" inflation pressures. The bank has subsequently revised its short-term inflation forecast for Q2 2026 upward to 4.2%, citing the combined impact of supply chain disruptions and the energy price shock.

Geopolitical Volatility and US Trade Policy

The central bank’s decision to hold rates reflects a deteriorating global trade outlook. Ongoing conflict in the Middle East has created a ripple effect through New Zealand’s economy, primarily via the cost of imported energy. Finance Minister Nicola Willis has warned that inflation could climb "much higher" if these tensions persist, potentially keeping the CPI outside the RBNZ’s 1-3% target band for an extended period.

Adding to the complexity is the RBNZ’s recent analysis of US trade policy. A March 2026 Analytical Note highlighted a bifurcated risk: while shifts in US policy might offer short-run disinflationary effects, the long-term outlook points toward inflationary pressures driven by global supply chain inefficiencies and increased protectionism.

To mitigate these risks, New Zealand is aggressively pursuing trade diversification. On April 27, 2026, New Zealand and India signed a comprehensive free trade agreement. This landmark deal is intended to deepen economic ties and provide Kiwi exporters with more resilient market access as traditional global trade routes face increasing uncertainty.

Market Reaction and the Road to September

For financial markets, the RBNZ’s hawkish pause suggests that the era of rate cuts has ended for the foreseeable future. The Kiwi economy is currently walking a tightrope; while economic growth is slowing—a factor that usually encourages lower rates—the resilience of inflation has forced the MPC’s hand.

Analysts are now recalibrating their expectations. A growing number of economists anticipate that the RBNZ may be forced to pivot toward tightening later this year to anchor inflation expectations. Some forecasts now suggest an OCR hike as early as September 2026, with the rate potentially ending the year at 2.75%.

Comparison with Australia

The situation in New Zealand offers a stark point of comparison for the Reserve Bank of Australia (RBA). While the RBA currently maintains a higher cash rate, both nations share a vulnerability to the same global commodity shocks. The RBNZ’s struggle to bring inflation back to the 2% midpoint despite a significant tightening cycle in 2023-2024 serves as a cautionary tale for Australian policymakers navigating similar supply chain disruptions and energy price volatility.

Related Articles

Comments

0Loading...

No comments yet. Be the first to share your thoughts.