RBNZ Survey Shows Significant Rise in Short-Term Inflation Expectations

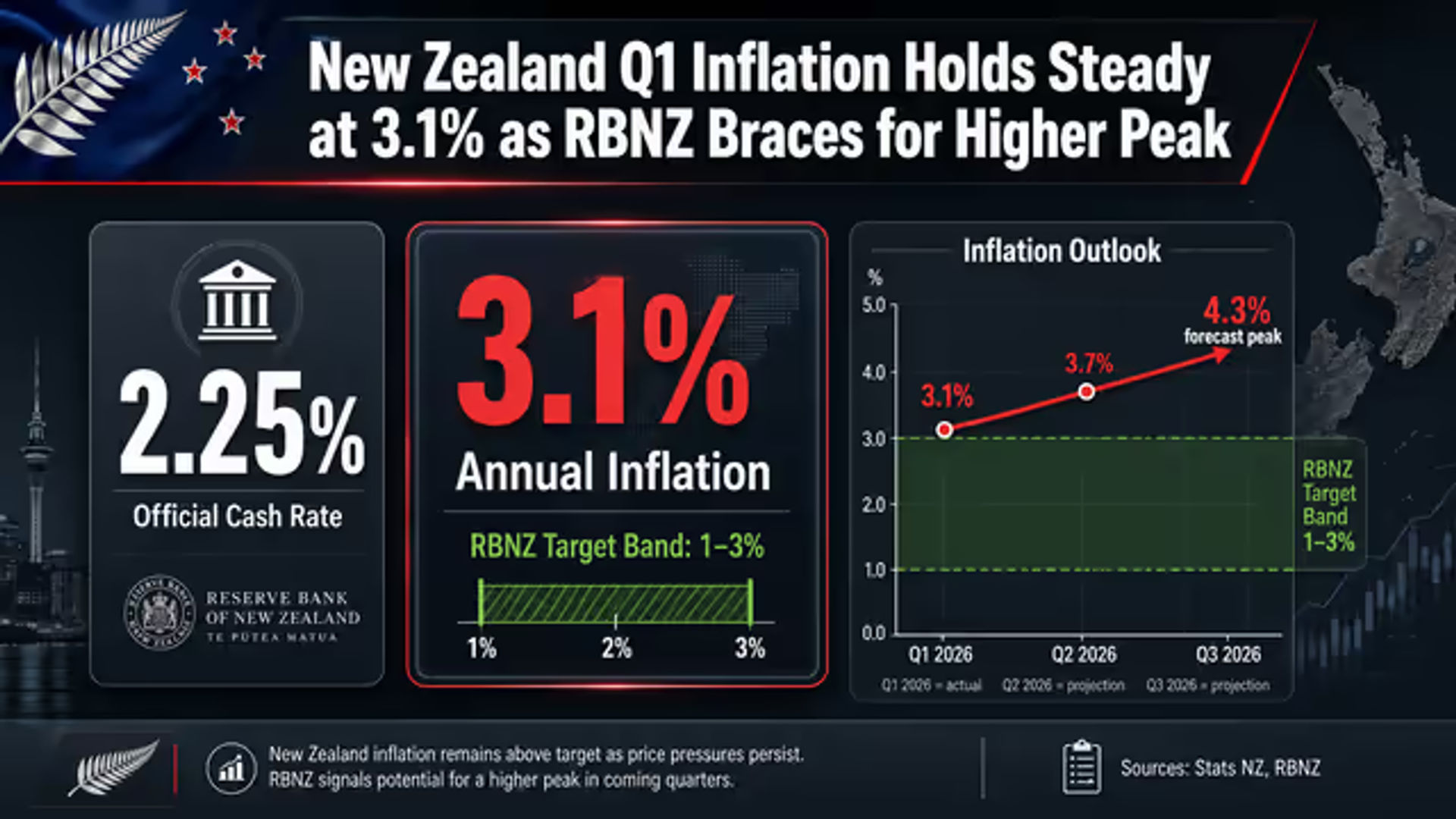

The Reserve Bank of New Zealand released its Quarterly Survey of Inflation Expectations on Wednesday, 13 May 2026, revealing a sharp increase in short-term inflation forecasts. The data shows that one-year-ahead CPI inflation expectations have jumped to 3.41%, up from the previous 2.59%. Simultaneously, two-year-ahead inflation expectations rose from 2.37% to 2.53%, marking the highest level for this specific metric since the fourth quarter of 2023. These results arrive at a critical juncture for the Reserve Bank of New Zealand as it evaluates whether recent accelerations in consumer prices are becoming a permanent fixture in the nation's inflation psychology.

This upward shift in expectations follows recent data from Stats NZ on 21 April 2026, which confirmed that annual CPI inflation for the first quarter of 2026 remained unchanged at 3.1%. This figure persists above the Reserve Bank of New Zealand target range of 1% to 3%, suggesting that domestic price pressures are more stubborn than previously anticipated. The survey results indicate that businesses and professional forecasters are bracing for a period of sustained price growth, even as longer-term outlooks show a different trend. While short-term figures climbed, five-year-ahead inflation expectations decreased to 2.22%, and ten-year expectations fell to 2.19%, suggesting a belief that current pressures may eventually subside over a longer horizon.

Monetary Policy and Interest Rate Outlook

The surge in inflation expectations has immediately influenced the outlook for the Official Cash Rate. The mean expectation for the Official Cash Rate at the end of June 2026 has increased to 2.34%, up from the previous estimate of 2.25%. More significantly, the one-year-ahead expectation for the Official Cash Rate has jumped to 3.01% from a previous 2.58%. This hawkish shift in sentiment suggests that market participants now anticipate a more aggressive tightening cycle to combat persistent price increases.

Financial markets have reacted to these developments by fully pricing in a rate hike from the Reserve Bank of New Zealand for July 2026. The Overnight Indexed Swap market currently anticipates two separate rate hikes by September 2026. This shift comes as the Reserve Bank of New Zealand prepares for its next Monetary Policy Statement on 27 May 2026, which will be followed closely by the New Zealand Budget announcement on 28 May 2026. The New Zealand Dollar showed limited immediate volatility following the survey release, with the NZD/USD pair trading at approximately 0.5950.

Economic Growth and Labour Market Projections

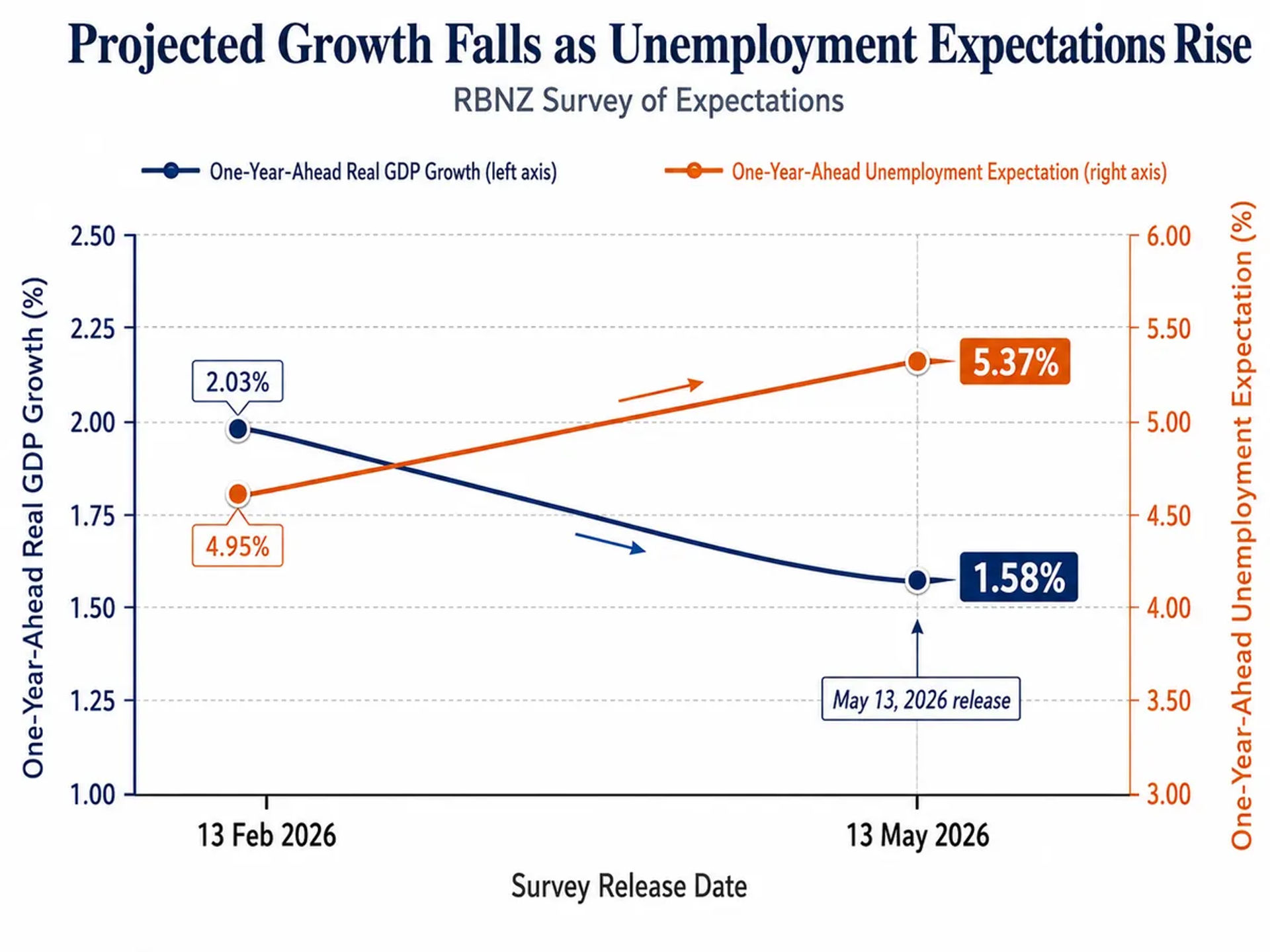

While inflation expectations are rising, the outlook for economic activity appears to be softening. The survey indicates that one-year-ahead real GDP growth expectations have declined to 1.58%, down from the previous 2.03%. Two-year-ahead GDP growth expectations also eased, moving from 2.30% to 2.16%. This combination of rising inflation and slowing growth presents a complex challenge for policymakers, as traditional tools to curb inflation often further dampen economic expansion.

The labour market is also expected to experience a cooling effect. One-year-ahead unemployment rate expectations have increased to , up from , while the two-year-ahead unemployment rate is projected at . These figures reflect a growing concern that the current economic environment, characterised by high costs and restrictive monetary policy, is beginning to impact employment stability across the country.

Related Articles

Comments

0Loading...

No comments yet. Be the first to share your thoughts.