New Zealand Housing Consents Record First Annual Increase in Three Years

New Zealand's residential construction sector has reached a significant turning point, recording its first annual increase in new home consents after three consecutive years of decline. For the year ended March 2026, a total of 37,813 new home consents were issued across the country. This figure represents an 11% increase compared to the year ended March 2025, signalling a stabilisation and nascent recovery in the housing supply pipeline.

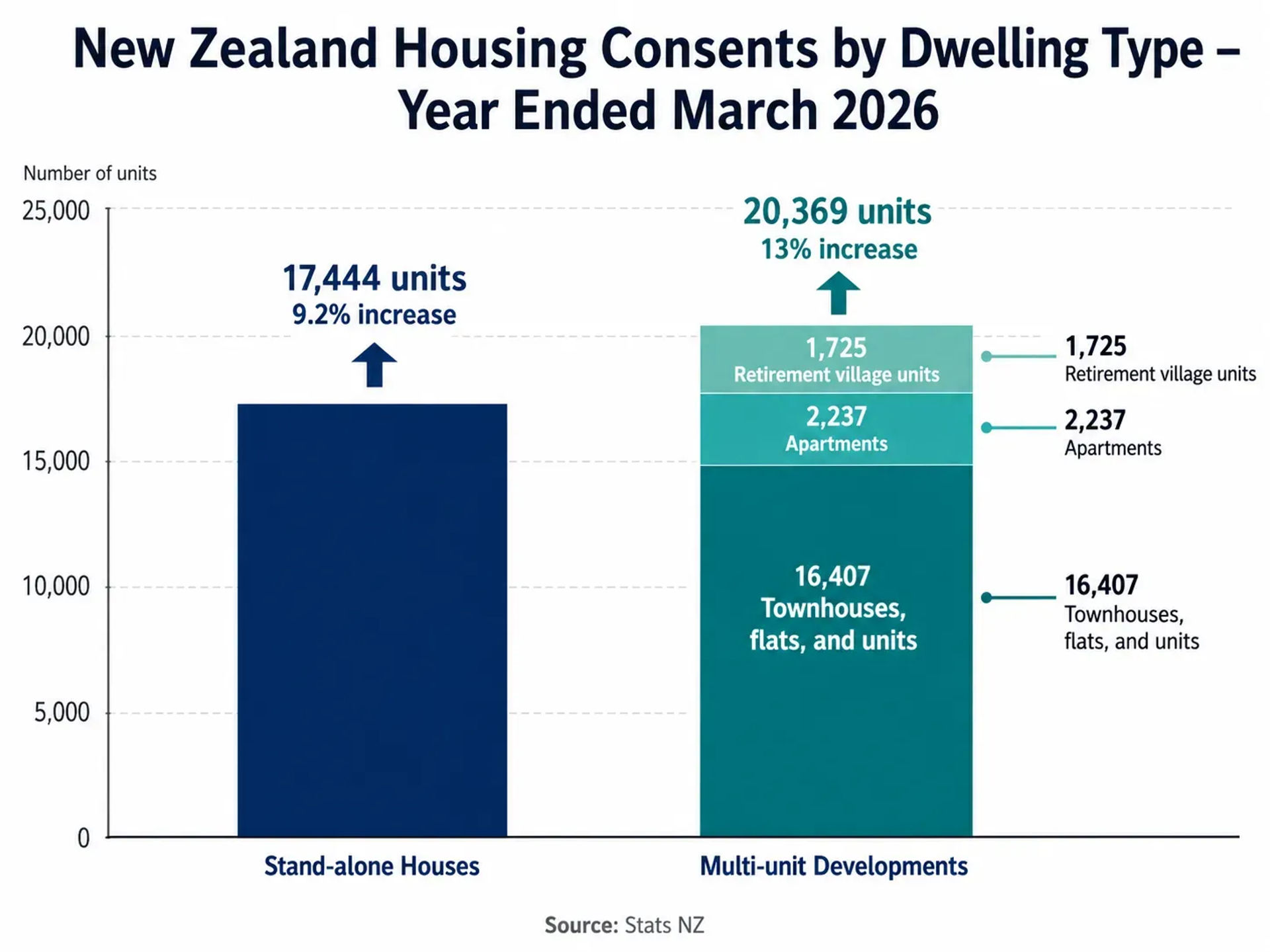

The growth in consent numbers was distributed across both traditional housing and higher-density developments. Stand-alone house consents rose by 9.2% to reach 17,444 units. However, the most substantial growth occurred in the multi-unit development sector, which saw a 13% increase to 20,369 consents. This category includes townhouses, flats, units, apartments, and retirement village units, reflecting a continued shift toward intensified urban living and specialised housing for the ageing population.

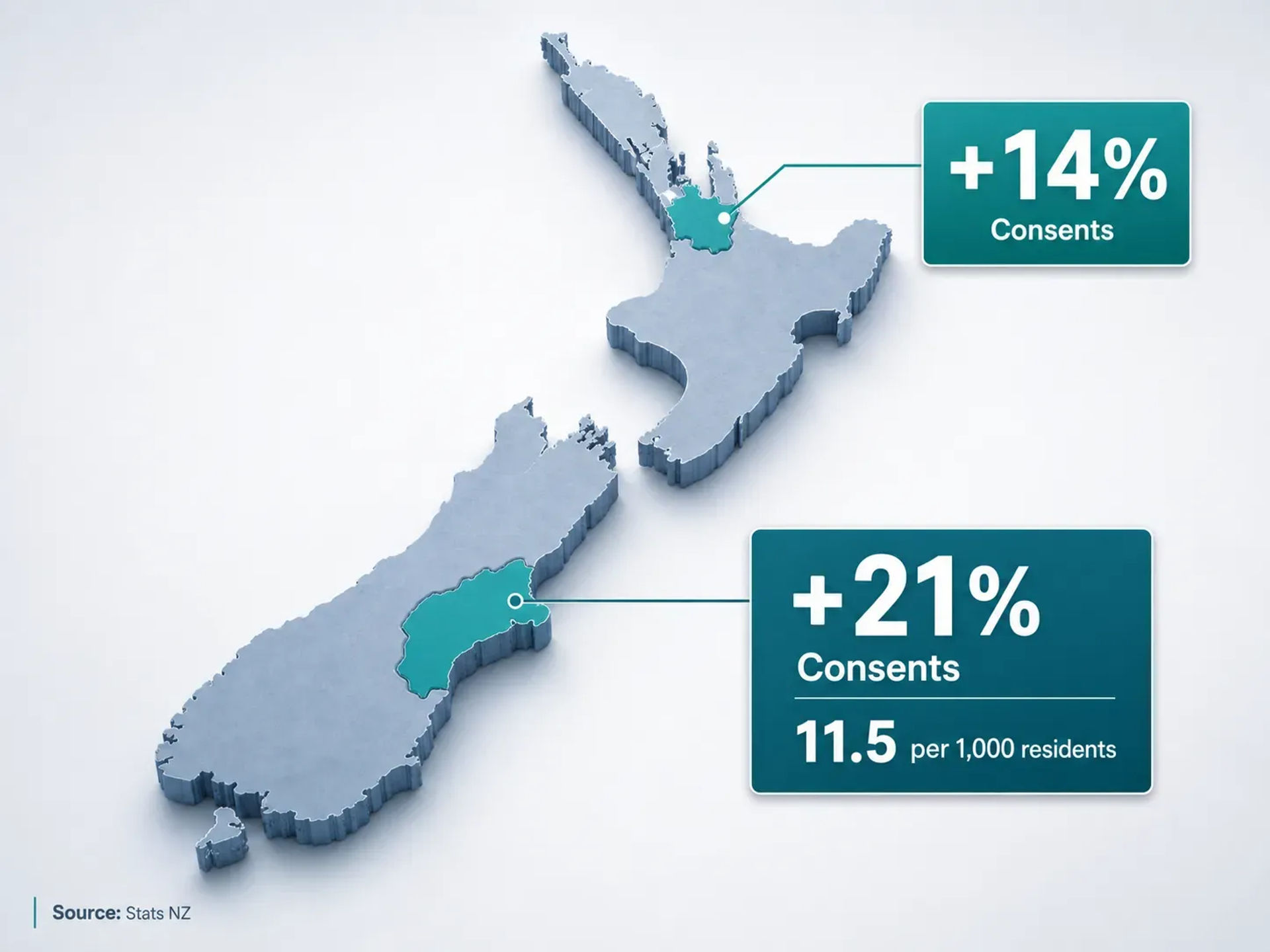

Regional data highlights a surge in activity within New Zealand's major population centres. Auckland recorded a 14% increase in new dwelling consents over the 12-month period. Canterbury experienced an even more pronounced rise of 21%, cementing its position as a primary driver of national construction activity. On a per capita basis, Canterbury led the nation with 7.1 new dwellings consented per 1,000 residents in the year to March 2026.

This annual recovery follows a prolonged period of contraction in the building sector. After reaching a peak of over 51,000 consents in the 12 months to May 2022, the industry experienced a sustained downturn between 2023 and 2025. The cycle appeared to find a base in August 2025, when annual consents sat at approximately 34,000. By the year ended November 2025, the recovery was beginning to take shape with a 7.0% increase to 35,969 units, eventually culminating in the 11% annual growth confirmed in the latest figures released on 30 April 2026.

While the annual trend is positive, more recent monthly data suggests that the recovery remains sensitive to economic conditions. In March 2026, the seasonally adjusted number of new dwellings consented actually fell by 1.3% compared to the previous month. This volatility comes as the sector faces renewed pressure from rising costs. Residential building costs increased by 0.9% in the fourth quarter of 2025, the largest quarterly rise since the third quarter of 2024, bringing the annual pace of cost increases to 2.3%.

Beyond residential housing, the non-residential sector also showed modest growth. The annual value of non-residential building work consented reached $9.0 billion in the year to March 2026, an increase of 1.2% over the previous year. This suggests a broad, if cautious, level of investment across the wider construction industry.

However, economists at Westpac have identified significant headwinds that may impact the momentum of new projects later in 2026. Satish Ranchhod and the Westpac economics team have noted that rising fuel and material costs are beginning to weigh on the sector. These increases are being driven by global conflicts, particularly in the Middle East, which have disrupted the building product supply chain. These external pressures, combined with general inflation, are expected to influence future project initiation and developer confidence.

Related Articles

Comments

0Loading...

No comments yet. Be the first to share your thoughts.